The folks at Redfin have been thinking a lot lately about how the world will look when the recession is over. Last Tuesday, we said that the Internet will shift toward applications that consumers will pay for rather than media content. Yesterday, we looked at startup economics, and speculated that most of the carnage is ahead of us, not behind us.

But what about real estate, where Redfin competes, the industry that got us into this mess? How will this industry be different after the recession?

Our take is that it will be much better, more efficient and more consumer-friendly too. It may come as a surprise that Redfin, long an outspoken critic of how brokers share data and serve consumers, is expressing support for the industry as it changes. But these changes are dramatic.

The Keys to the Kingdom

Just a week ago, at a meeting of all the big brokers in a major American city, the group went through every scrap of data that brokers have long kept for themselves and decided to publish nearly all of it online. It felt like that moment in the French Revolution when all the aristocrats volunteered one after the other to give up their estates.

This burst of openness is partly the result of the Department of Justice settlement with the National Association of Realtors, which with less fanfare than the original lawsuit, is going into effect across the nation this spring.

But many brokerages share listings through collectives not bound by the settlement, and those bound by the settlement often liberalized their policies further than the settlement required. So it has to be more than that.

Suddenly, An Industry That Wants to Change

Out in the field, the old battle-axes who once tried to scare off our clients aren’t interested much in fighting anymore and neither are we; for the first time in our history, we haven’t had a client complaint about hostility from a traditional real estate agent in months.

This detente is partly due to a more liberal Redfin tour policy, and perhaps a more temperate Redfin tone, but it is also due to a shared sense of peril, and a new commitment to reform.

At the industry’s big real estate conference, where only three years ago we had been jeered for the simple statement that “our goal is to make real estate more efficient,” the conference founder told the assembled brokers last January that it was time to change: how agents are paid, what data we share, how much we charge.

It’s happening in lending too, big-time. Banks for example are clamping down on inflated appraisals, kickbacks and closing credits: it used to be you could get $10,000 extra at closing by asking the seller to raise his price and then give you the extra amount in cash at closing. In effect, the bank was loaning you an extra $10,000 based on an inflated appraisal. Just last week, we saw a deal like this torpedoed by the bank. It’s exactly the kind of deal that should have never been possible.

The Hyper-Buyers

Consumers are getting smarter too. We have now seen the ascendance of Hyper-Buyers, folks who develop their own Black-Scholes-style models and Excel spreadsheets, who dig into county tax records and zoning ordinances on the Web, who have mastered the lingo of short-sales, trustee auctions, REO purchases. They’re younger than ever before, because older folks are trapped in the home they already have. They think for themselves. And they drive a hard bargain.

The data consumers now want isn’t limited to the listing. They also want the goods on their agent, their lender and everyone else they’re counting on to get them a good deal. Folks can now assess an agents’ or lenders’ performance just as they would a restaurant on Yelp, but with more objective data.

The Brain Drain

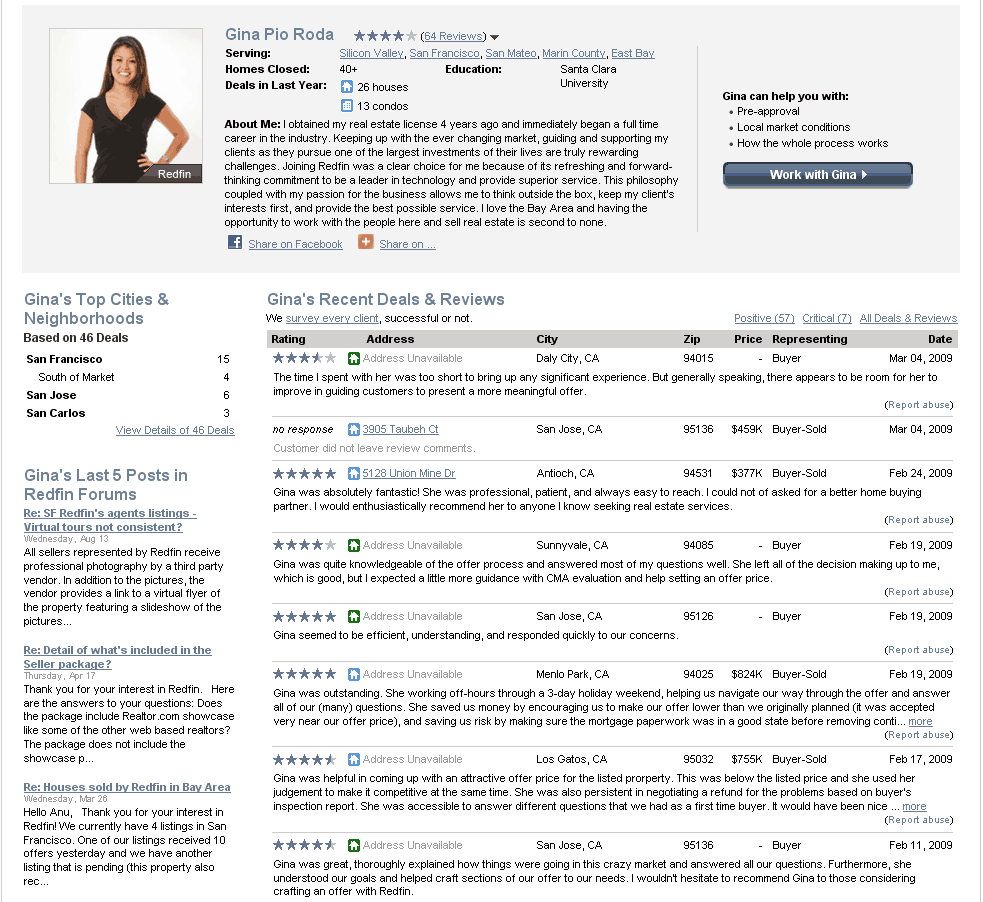

This will increase the stakes in online real estate. I’m always surprised in looking at other sites how little energy is spent in guiding consumers’ choice of agent: many agent profiles are nothing more than a blurb, a telephone number, and a photo.

We can do better, showing all the deals an agent did and what customers said about him. After all, we’re not only trying to sell a house online but also an agent’s service — a fact which Redfin was slow to recognize.

Where will the money come from to build all this?

It seems unfair that the unspent portion of $100 milllion+ in venture capital that flowed into real estate from 2006 to 2008 will now have a disproportionate impact on the rest of the industry, which may no longer have the money to build the best real estate websites. At a penny-pinching time, we worry that traditional brokers like Century 21 and Coldwell Banker will outsource their brains to venture-funded companies.

The companies that raised the most capital — Redfin is not necessarily among them — will be like one-eyed men in a world of blind people: they will be kings.

The $24,000 Question: Do Real Estate Websites Really Matter

But larger than any concern about whether brokerages will run their own websites is our concern that it really won’t matter who has the best website, because many consumers will just make real estate choices based on personal relationships.

This is online real estate’s $24,000 question.

If most folks never make the leap from a website to a real estate agent — whether through an ad on a real estate media site or through Redfin’s whole home-buying application — then all the tech-driven businesses are in trouble.

Three years in, Redfin is still growing through the downturn, so we obviously feel that the web will drive purchasing decisions in real estate as it does in other areas of the economy. Like never before, people are signing up for home tours through our home-tour wizard, and contacting our agents after viewing their online profiles.

But we have to grow very fast to be able to fund such a large R&D cost. So far, this has worked out reasonably well, but it has always been a perilous way to live.

If, at the end of this cycle, the new venture-funded websites haven’t really changed how consumers pick an agent — not two or three percent of consumers, but twenty or thirty percent of them — venture capitalists will conclude that real estate really is an industry impervious to structural change, leaving us alone until the next big bubble.

Either Way, The Consumer Wins

We think that this time around, the industry really will change. Surprise, surprise. Whether online players become large or small, the mere presence of alternative sources of information and business models is already making the industry more transparent and efficient, in the same way that Southwest affects how consumers fly on other airlines. (We have long wanted to measure whether there is a similar phenomenon, a Redfin effect, in the markets we enter.)

We know that one day when real estate prices come back, all the scam artists and flim-flam men will come back too. But by then the web will have shifted the balance of power so far in consumers’ favor that it won’t matter. Do you share that hopeful outlook? Leave a comment and let us know. We’re always listening…

United States

United States Canada

Canada