Which comes first, the house or the homebuyer?

These days, it’s the homebuyer. The Federal Reserve kept a lid on interest rates today, citing the housing market’s slow recovery as a cause for concern. Chair Janet Yellen said housing is “very depressed” and “demand for housing should be there.”

She has it backward. There’s plenty of demand for housing. What’s missing is supply.

Look at homebuilders, a small but important part of the economy. More than anyone, they’re still haunted by the financial collapse, which put trade schools out of business and dried up credit. All these years later, builders can’t find skilled construction workers, can’t get loans to buy lots and are having harder time getting permits from resource-strapped local governments.

Goldman Sachs calls it a list of “hard constraints”. In other words, even if builders wanted to put up more houses (and they do), they can’t. Which leaves us with strong demand and short supply.

“Yellen said housing demand isn’t where it should be, but what’s slowing down new construction isn’t the buyers, it’s the sellers,” Redfin Chief Economist Nela Richardson said. “Builders and developers are in a logjam right now because of what went down.”

It’s turning around, but slowly. Industry optimism is at its highest in a decade, according to the National Association of Homebuilders. Companies are encouraged by foot traffic and sales, but that’s not yet translating to more construction.

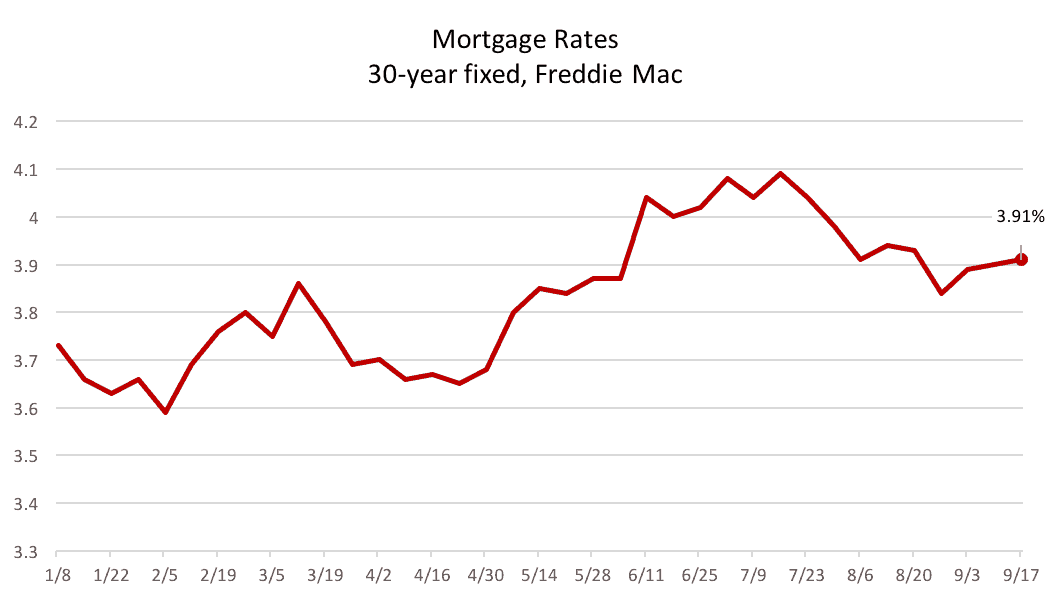

For now, the Fed is keeping interest rates low. Today, the cost of a 30-year, fixed rate mortgage is still below 4 percent. That’s good for buyers–and demand.

United States

United States Canada

Canada