The housing market sent some mixed signals on the eve of the industry’s busy season. Yesterday we learned that sales of existing homes—those pre-owned properties that account for most of the market—took a nice pop in March, jumping 10.4 percent from a year ago, the biggest increase since August 2013.

The housing market sent some mixed signals on the eve of the industry’s busy season. Yesterday we learned that sales of existing homes—those pre-owned properties that account for most of the market—took a nice pop in March, jumping 10.4 percent from a year ago, the biggest increase since August 2013.

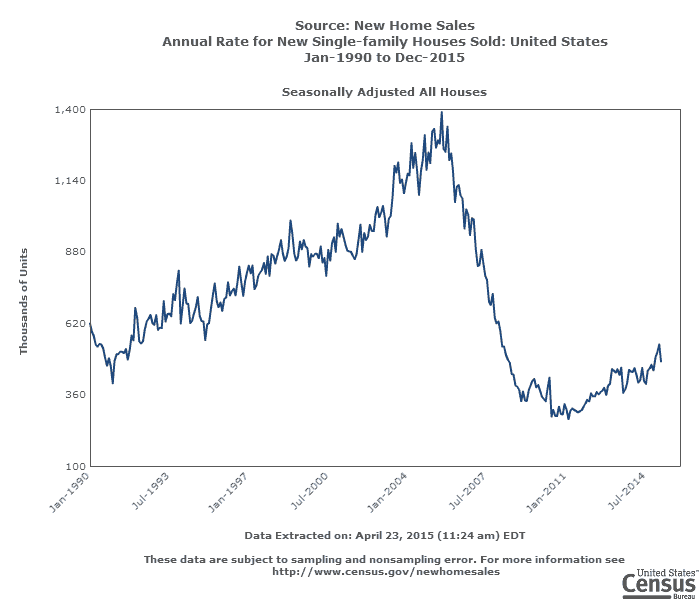

Today we heard a different story. New home sales in March were far below what most economists expected, reaching a pace of 481,000 a year instead of the anticipated 515,000, the Commerce Department reported. While newly built houses and condominiums make up less than 10 percent of the overall market, they’re important for two reasons: Construction creates jobs and gives a healthy boost to the overall economy, and the nation’s housing stock is far below where it needs to be.

That lack of inventory is a particularly worrisome thing, especially as millennials are growing up and moving out on their own. Add growing demand to weak supply and you get rising prices. That’s what’s happening, and it’s preventing young adults and moderate-income households from owning homes. The pace of new home sales is below where it was 20 years ago.

Where will people live? Rents aren’t much better, and wages haven’t kept pace. Parents’ basement, anyone?

Today's Housing Data: One Reason You're Stuck in Your Parents' Basement

April 23, 2015 by Lorraine Woellert, Makayla Zurn, Luis Mojica and Suzanne Harrison

Updated on October 6th, 2020

United States

United States Canada

Canada