Over Half of Homeowners are Not Currently In a Financial Position to Sell

From Austin to Boston to Chicago, low inventory continues to be a key point of frustration in the housing market. Buyers don’t see enough options, sellers are afraid to list without having a new home and agents anticipate another competitive season.

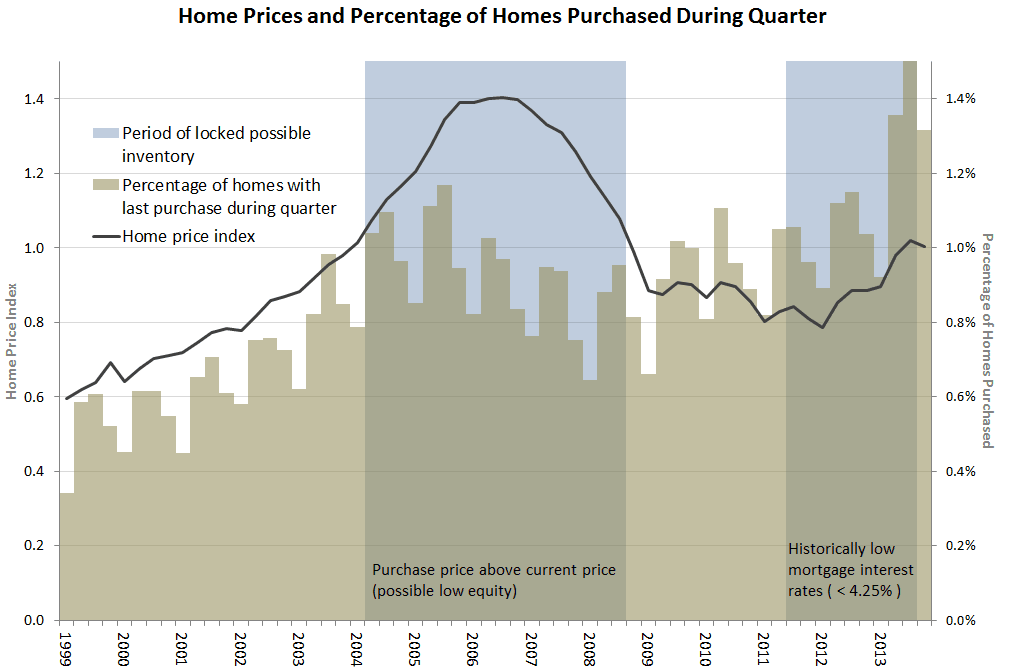

How did we get here? The dearth of homes for sale is the result of two phenomena: people buying homes at the peak of the housing boom, paying more for them than they are now worth; and, after the bust, people buying and refinancing homes at unsustainably low interest rates.

In this study, Redfin has uncovered four categories of homes that are unlikely to reach the market anytime soon (percentage of homes affected indicated in parentheses):

- Low equity (19%) — A home with low equity is one for which the homeowner owes more than 80% of the value of the home. Most of these low equity homes were purchased or refinanced during the home price bubble between 2004 and 2009.

- Low mortgage rate (16%) — Homes purchased or refinanced when national mortgage interest rates were lower than 4.25 percent are considered to have low mortgage interest rates. These purchases and refinances occurred between 2011 and 2013.

- Company or investor owned (3%) — These are homes currently owned by a company or investor who purchased five or more homes in a metro area during the past 10 years.

- Purchased or refinanced in the past seven years (14%) — The home has been owned by the current owner for less than seven years. Redfin has found that buyers typically sell after more than seven years.

Combining these factors, more than half of all existing homes are unlikely to be put up for sale without significant changes in the housing market.

Buyers and Refinancers With Low Equity

Many who bought between 2004 and 2009 paid more for their home than the home is now worth. Others purchased homes with little or no down payment. Additionally, many people refinanced during the bubble to cash out on the housing market gains while expecting prices to continue rising. If these homeowners sold their homes today, they may not pocket much profit to put toward their next home.

Buyers and Refinancers With Low Mortgage Rates

Between 2011 and 2013, mortgage interest rates hit historic lows. Many buyers and refinancers locked in rates well below 4 percent. These homeowners are unlikely to sell and buy something else because home prices and mortgage rates are now significantly higher than they were at the time that they purchased or refinanced their current home. Their mortgage payment would be 29 percent higher on the same home because of those rising rates and prices. Recently, the Institute for Housing Studies corroborated Redfin findings with evidence that “rapidly increasing interest rates, along with negative equity, ‘lock in’ households to their existing mortgages and residences, which reduces housing turnover.”

Miscellaneous: Recent Buyers, Companies and Investors

Fourteen percent of homeowners bought in the past seven years and have at least 20 percent equity in their home. The rule of thumb is that homes sell roughly seven years after their purchase. While they are financially ready to sell, their relatively recent home purchase means these owners are likely to stay put.

Finally, 3 percent of homes are currently owned by a company or investor. These investors are likely holding on to their investment for the capital appreciation and rental income.

A look at Inventory Across Metros

While the tight inventory situation is almost universal across the country, there is some variation across markets. Low equity and low mortgage rates have helped suppress inventory across much of the West, including Seattle, Sacramento, Denver and Los Angeles. The South and East are better positioned as far as home equity, and are subsequently seeing more homes for sale. Atlanta, Charlotte, Raleigh and Long Island all have a larger percentage of homes for sale than the rest of the country.

Inventory Will Remain A Challenge in 2014

Although some markets are bouncing back from their 2013 inventory lows, buyers in 2014 will continue to face limited options and competitive situations in most markets. Rising home values and new construction may help alleviate the low inventory problem in some places. Redfin calculates that all virtually all low equity homeowners could be in the black with five years of 5 percent price gains. Additionally, Redfin agents have already seen inventory rise in markets with significant home value appreciation, such as Southern California, Phoenix and Washington, D.C.

A Deeper Look at Housing Boom and Interest Rates

For those wanting to gain deeper insight into how these situations unfolded, here is a look at the most recent purchase and refinance transactions for current homeowners. By looking at these trends over the past 15 years, we can get a clearer picture of market conditions during the homeowners’ purchase or refinance. We’ve highlighted the two unusual periods — high home prices from 2004 to 2009 and low mortgage interest rates from 2011 to 2013 — which both contributed to lower inventory.

Methodology

Redfin looked at single-family home, condo and townhome transactions, mortgages and refinances since 1999, across 29 metropolitan areas and divisions. To establish overall inventory affected by each factor, Redfin looked only at the latest transaction on each home. We used the number of existing homes provided by county assessor offices as our denominator for all metrics.

United States

United States Canada

Canada