Key takeaways for the 4-week period ending August 9:

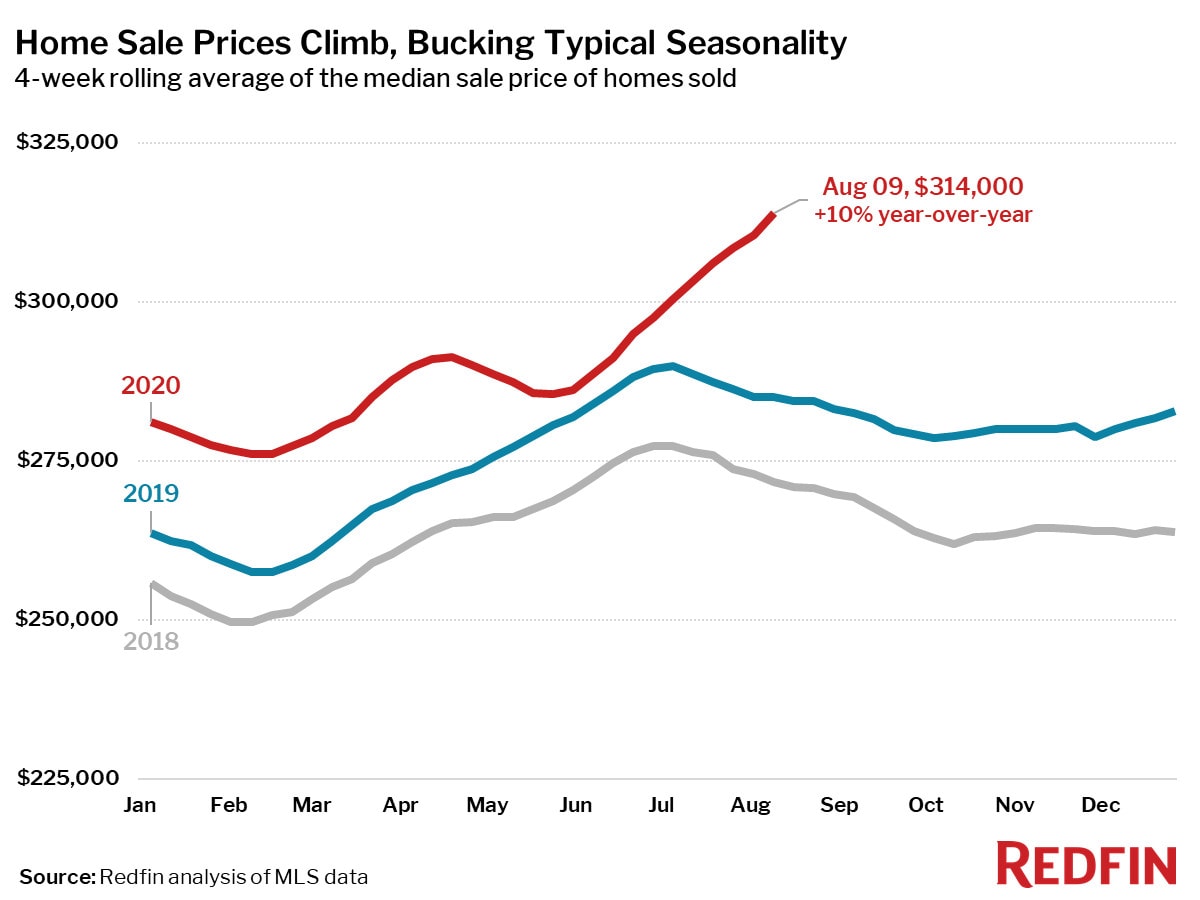

- Home sale prices were up 10% year over year—the largest increase in over six years—to another new all-time high of over $314,000. Prices keep climbing month over month, bucking typical seasonality.

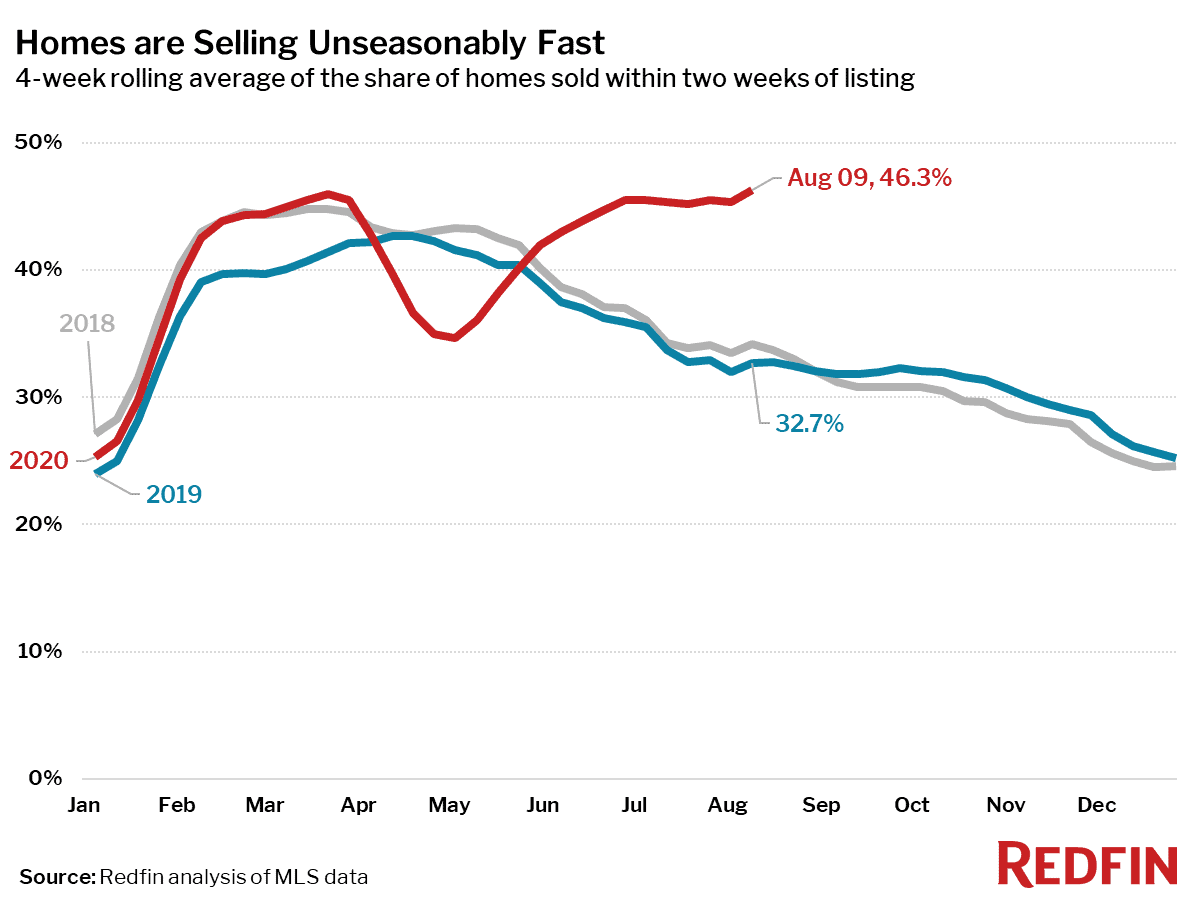

- 46% of homes had an accepted offer within the first two weeks on the market, the highest level since at least 2012 (as far back as our data on this measure goes). This measure is also increasing at a time of year when it usually falls.

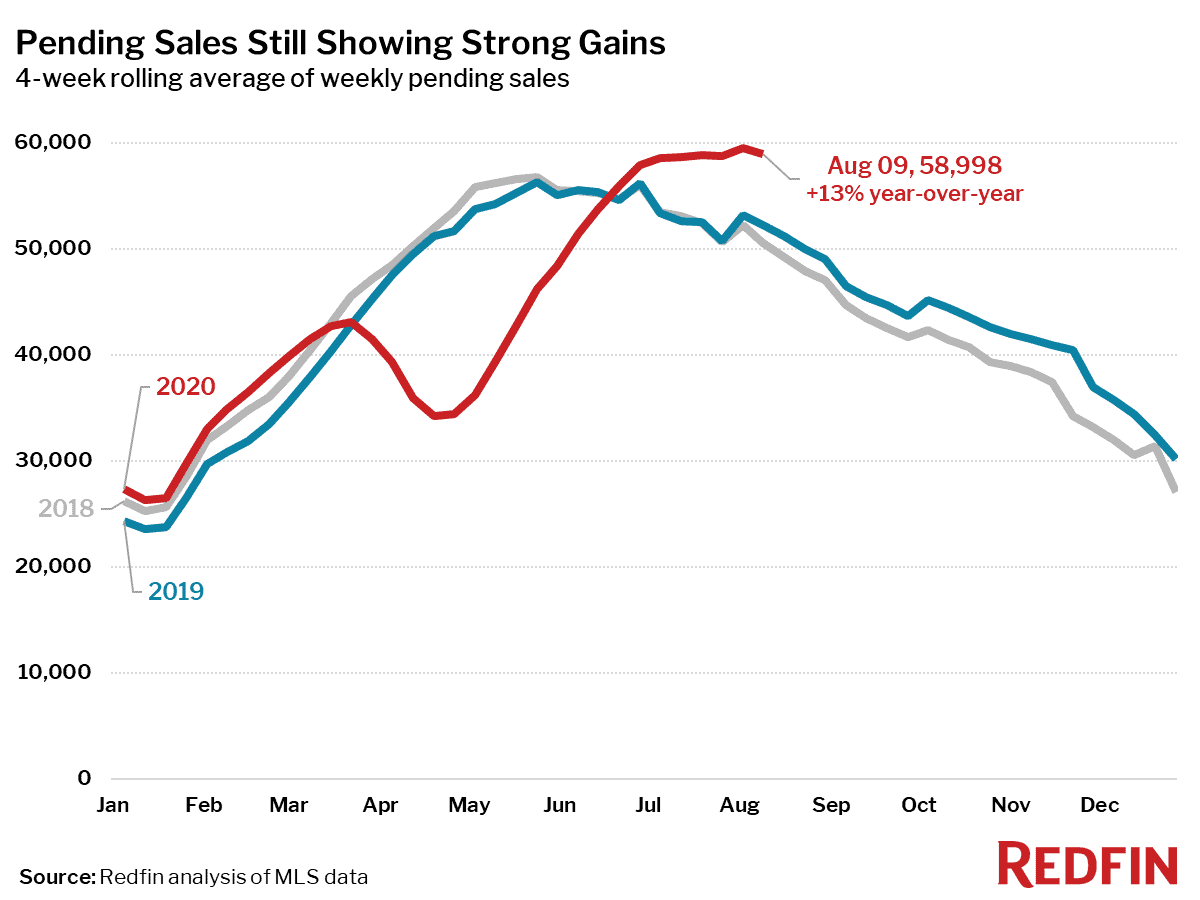

- Pending home sales were up 13% year over year, and have plateaued since early July, a time when sales usually begin to decline.

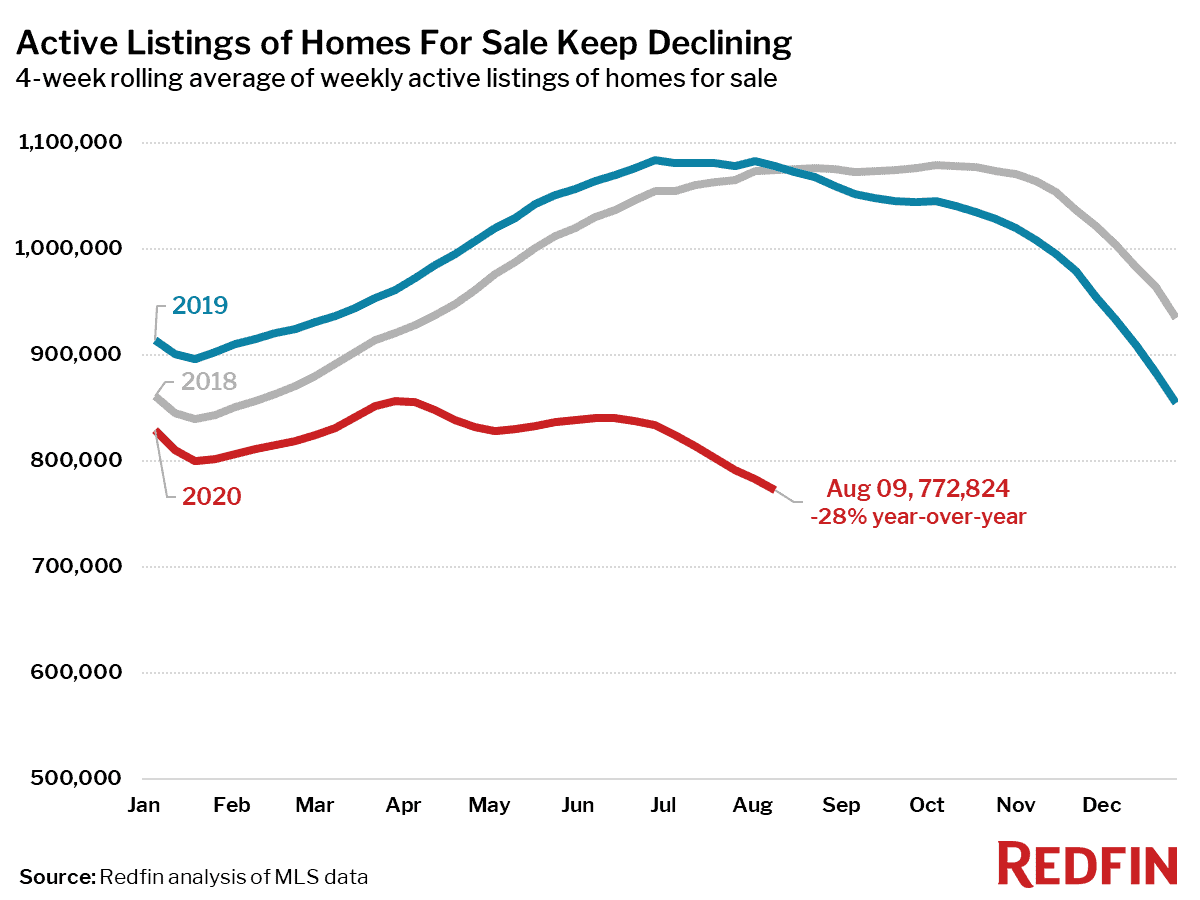

- The supply of homes for sale continued to fall; active inventory of homes for sale was down 28% year over year, but new listings were basically flat from 2019.

Seasonality is out the window this year

Home prices typically decline this time of year after hitting a seasonal peak in late June or early July. This year, as of the four weeks ending August 9, home prices were up 3.5% month over month. Last year home prices fell 1.7% over that same timeframe.

The median price of homes that sold during the four-week period ending August 9 was up 10% year over year—the largest increase in over six years—and hit a new all-time high of $314,000. In the last week of the period, prices were up 12% from a year earlier. Thanks to seemingly insatiable homebuyer demand, the typical seasonal patterns of the housing market have been short-circuited this year.

“With the coronavirus and the presidential election, things have been anything but typical this year,” said Spokane, WA Redfin agent Brynn Rea. “I don’t feel it slowing down at all right now like it usually does when people are typically spending more of their time on vacations and getting ready to go back to school.”

Homes are selling far faster than they typically do this time of year

Of homes that went under contract during the four weeks ending August 9, 46% found a buyer within two weeks of hitting the market—a slight uptick from the four-week period ending August 2 and the highest level we’ve seen since at least 2012 (as far back as our data is available). During the same period last year, 33% of homes found a buyer within two weeks.

“In Albuquerque we have a lot of people moving here from coastal cities, but if you were to call me today and say ‘I want to come down and see this list of five to 10 houses,’ there’s a good chance half of them won’t be available by the time you arrive,” said Albuquerque Redfin agent Jimmy Martinez. “We are not seeing the usual late summer slowdown. Instead, more homebuyers are touring homes.”

During the four weeks ending August 9 the share of homes that found a buyer in two weeks or less increased 2.0 percentage points from the previous month. Last year during that same period the share declined 3.0 percentage points.

One reason that the share of homes selling quickly is staying high when it typically declines is a surge in demand for some home types and locations that were largely considered undesirable pre-COVID.

“There’s not an area that isn’t hot right now because of a lack of homes for sale,” said New Jersey Redfin listing agent Darlene Schror. “Buyers today have a whole new set of preferences, such as being far away from neighbors and having space for a proper office, on top of all the usual criteria like highly rated schools. The houses that surprise me the most are the ones out in the boondocks, so far from the cities. You’ve got to drive to everything; there’s nothing to walk to. Before the pandemic, nobody wanted that stuff. Homes listed in those areas would sit on the market for a long time. Now they are hot.“

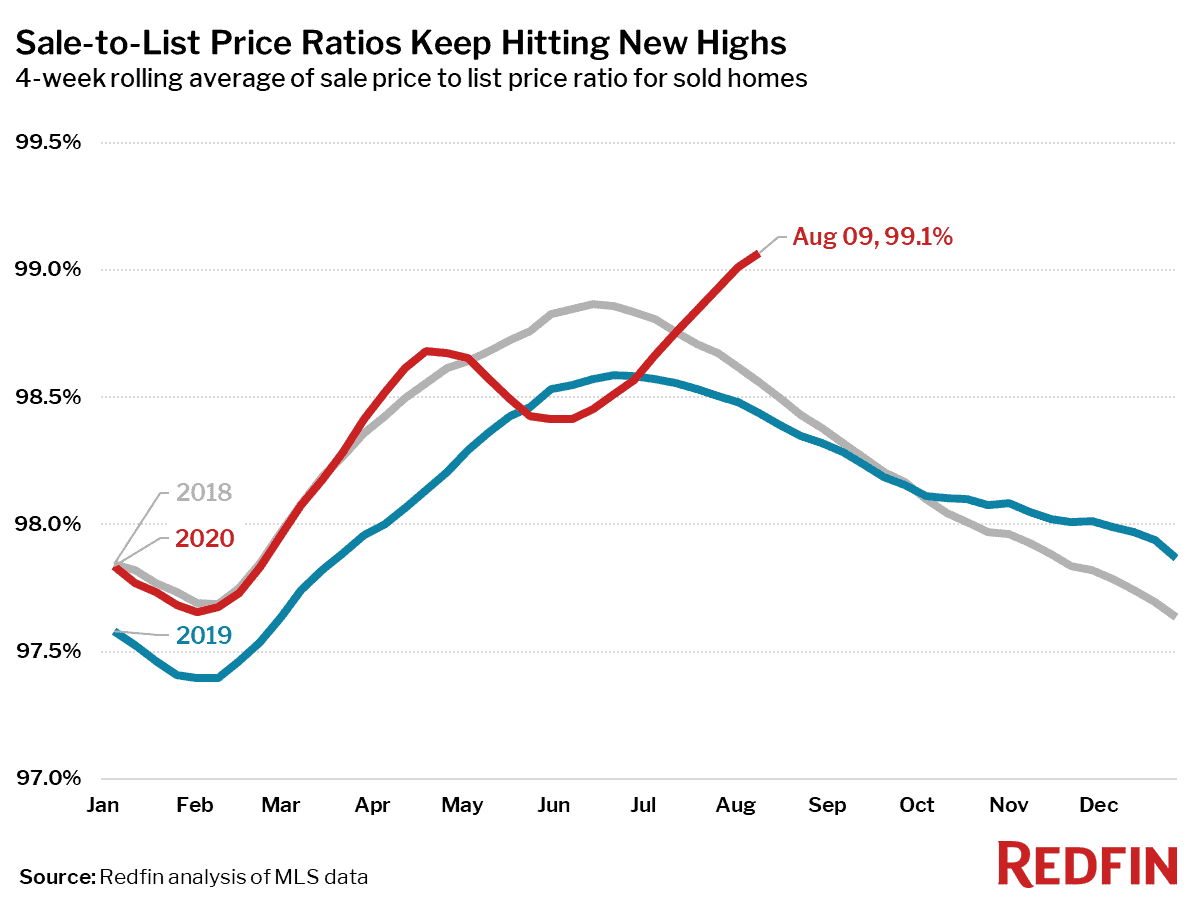

The average sale-to-list price ratio increased to a new record high of 99.1%–meaning homes are selling closer than ever to their list price–up from 98.4% during the same period last year. Month-over-month this measure has increased 0.3 percentage points. Typically during this time of year the sale-to-list ratio also declines—it fell 0.1 percentage points in 2019 and 0.2 percentage points in 2018.

Demand is plateauing instead of falling

For the week ending August 9, the seasonally adjusted Redfin Homebuyer Demand Index was up 31% from pre-pandemic levels in January and February. Pending home sales for the four-week period were up 13% compared to a year earlier. Month over month, pending sales were essentially flat, up 0.6%. Pending sales have been plateauing near their 2020 peak since early July. Contrast that with the same period in 2018 and 2019, when pending sales fell an average of 2.7%.

Supply of homes for sale is down, down, down

Active inventory of homes for sale was down 28%, while the number of new listings was basically flat year over year for the four-week period ending August 9 (-0.5%).

“Right now you have a set of people who are highly motivated to buy — they have the money and they have the desire, and they aren’t afraid of competition,” said Redfin chief economist Daryl Fairweather. “But there is an even bigger set of homeowners who are very comfortable where they are and don’t want to rock the boat. Some simply don’t want to deal with the hassle of moving during a pandemic and facing competition when they buy. Others may be struggling financially, but they are protected right now by mortgage forbearance, so they want to hold onto the equity in their homes in case the government doesn’t come through with additional assistance. That imbalance between people who want to buy and people who want to sell is driving up prices.”

The fact that new listings are only just even with last year’s levels and not climbing higher suggests that the homes that might have been put up for sale in the spring are just “lost inventory”—there isn’t pent-up supply that will flood the market to make up for them. The number of homes for sale keeps dropping, each week setting a new low point since the National Association of Realtors and the government began tracking this data in 1999.

However, homebuyers may soon see some relief to the inventory crunch thanks to a new 0.5% fee added to mortgage refinances starting September 1. This fee only applies to refinances and not home purchases, so homeowners who want to take advantage of low rates will have a financial incentive to sell their home and buy a different home. Because of this, some homeowners who have been reluctant to sell this year may choose to list their homes. Of course, this could also lead to more demand for homes when those sellers buy again. Therefore, we will likely see new listings and home sales both climb higher after the rule goes into effect.

“A lot of people are calling me now to sell their investment property or second home,” said Austin, TX Redfin listing agent Carmen Petersen. “What we’re not seeing much of lately is home sellers who are also looking to buy.”

Hope for a second stimulus fades

Without clarity from Congress on the future of its economic stimulus plan, there are serious risks on the horizon for the U.S. economy and the housing market. So far real estate has been one of the most resilient parts of the economy, but without additional government aid to make up for the lost consumer spending from millions of lost jobs and business closures, it is possible that larger economic fallout is on the horizon. If the economy gets a lot worse and mortgage forbearance expires, we could see a large wave of homes hit the market simultaneous with a drop in homebuyer demand, quickly flipping the supply and demand equation and driving home prices down.