Nine years ago this month, home prices posted their first recorded year-over-year drop, one of the earliest signals that the market was going south after years of dizzying growth. A year later, the recession was in full swing and President Barack Obama was being sworn into office.

When Obama gives his final State of the Union address to Congress tonight, he’s unlikely to make more than a passing nod to the state of the nation’s housing market.

So we’ll do the talking for him. Housing shoved the economy over a cliff into the downturn, but we also have it to thank for dragging us out. Here are nine measures of the good and bad of our nine-year recovery.

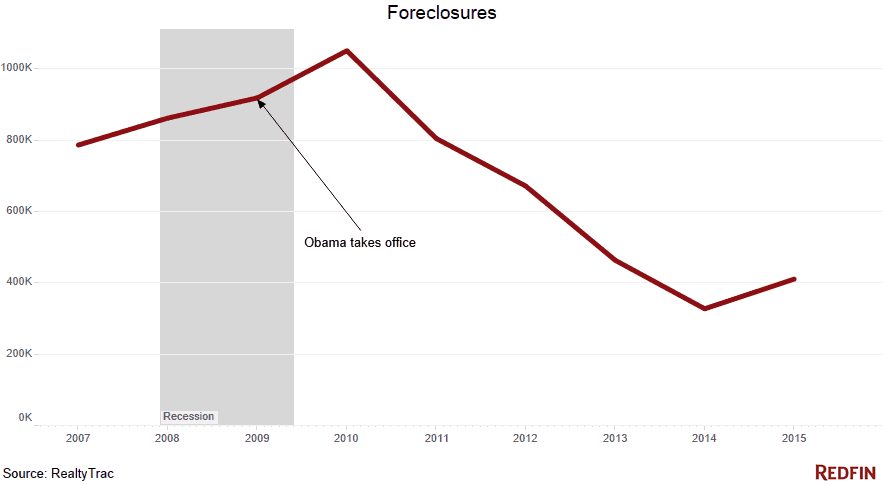

1. The Foreclosure Crisis Is Over

The after-effects of the bust linger as banks work through the last of the bad bubble-era loans, but the tidal wave has washed over. New foreclosures are at 2005 levels, according to RealtyTrac.

2. Americans Are Less Likely to Own

About 63.5 percent of households own a home, down from nearly 68 percent at the start of the recession. It might not seem like a big difference, but the rate of homeownership is lower now than it was in the 1970s, according to the Census Bureau.

3. Mortgage Rates Have Made History

As prices fell after the collapse, so did interest rates. In 2007, a 30-year mortgage went for more than 6.3 percent. Last week you could get one for 3.97 percent, according to Freddie Mac. That’s been a boon to affordability and an important driver of sales and price gains.

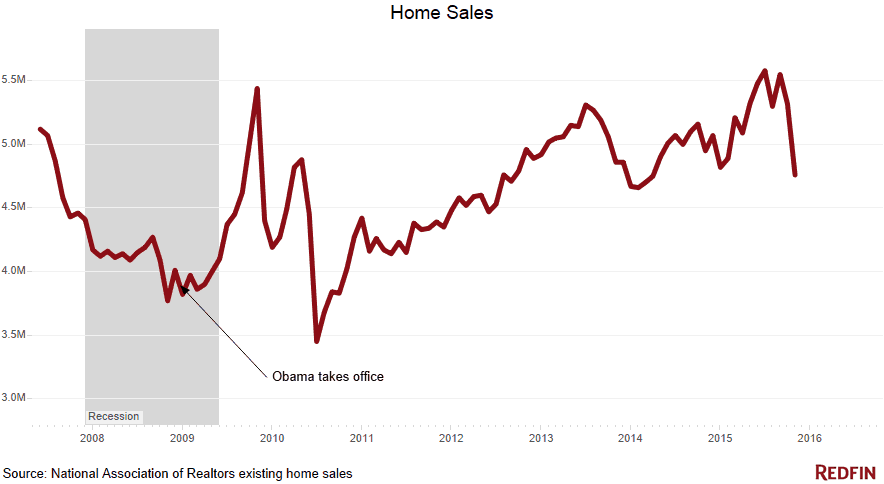

4. Buyers Are Buying

Excluding new construction, we’re on pace for 4.76 million home sales in 2015, according to the National Association of Realtors. It could be better. Homebuyer demand is strong and sales would be stronger if there were more properties on the market and more people could get loans.

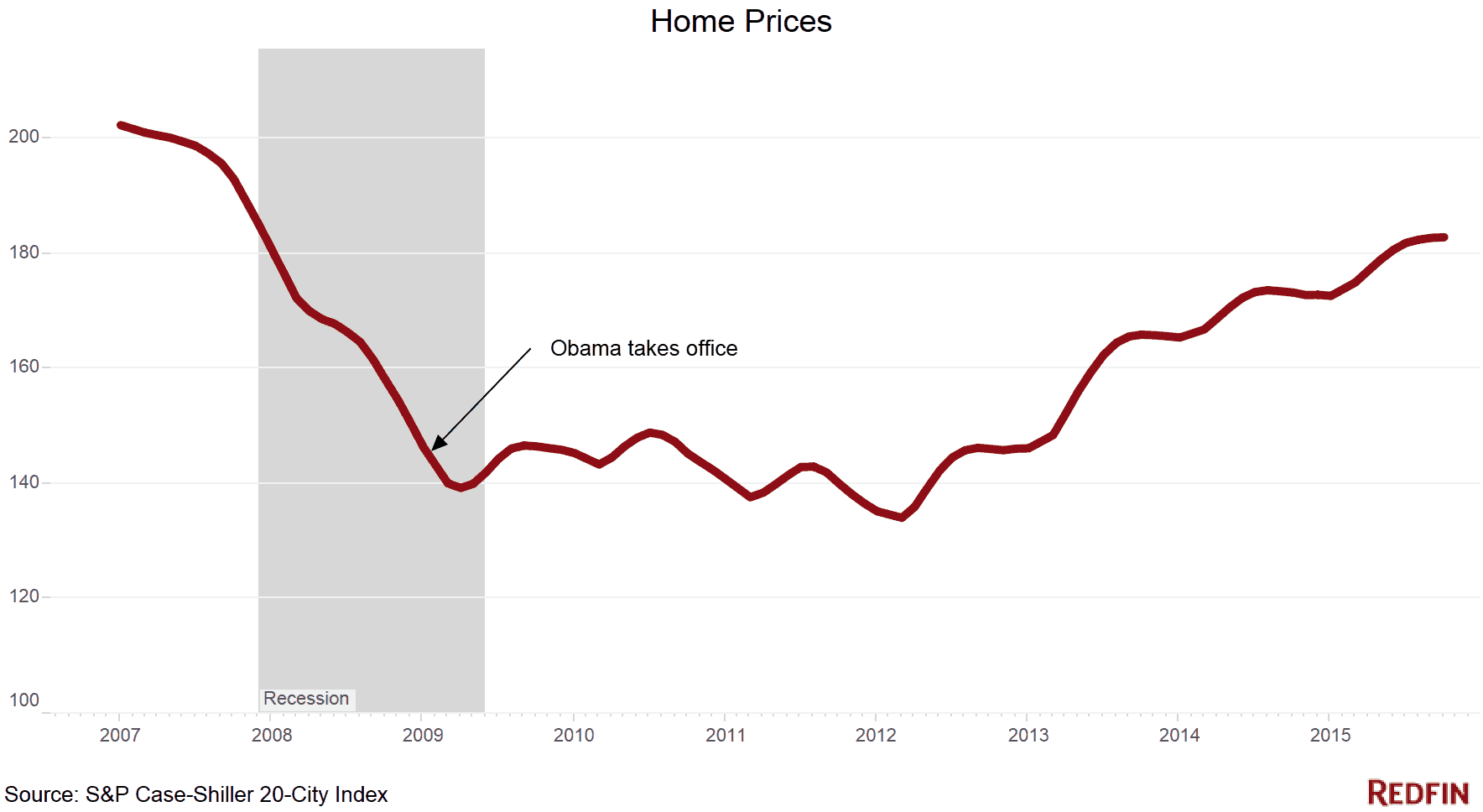

5. Prices Are Back

Nationally, home prices are 11 percent to 13 percent below their 2006 peak, according to S&P/Case-Shiller. In most major cities, including San Francisco and Denver, they’ve recovered completely. It’s been a slog, but we’re getting there.

6. Home Equity Is Back, Too

When home prices cratered, it wiped out a lifetime of wealth for many Americans. Now, not only are prices up, homeowners are borrowing a lot less, which has pushed home equity above pre-recession levels to more than $11.3 trillion in 2014, a 75 percent increase from the 2011 trough, according to the Federal Reserve.

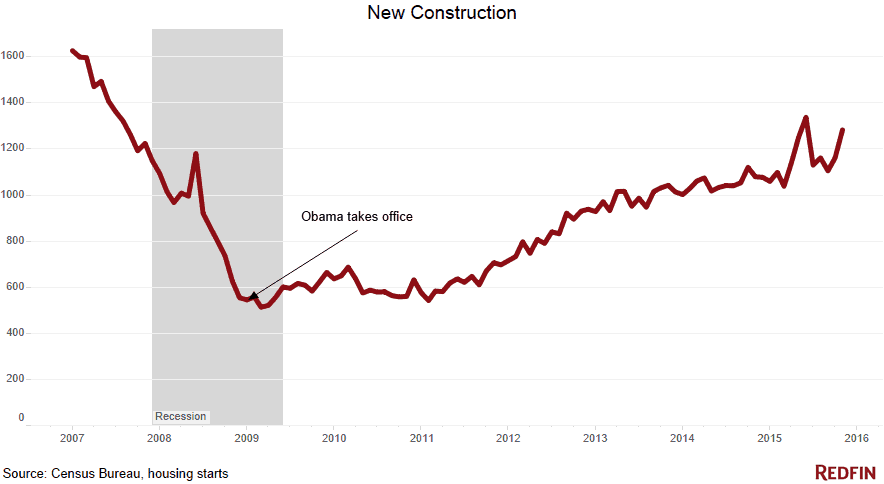

7. Builders Aren’t Breaking Ground

Last we checked, homebuilders were on track to construct fewer than 1.2 million houses, townhomes and condos in 2015, well below the 1.6 million the country needs to keep up with population growth and new households. That’s one reason homebuyers have so little to chose from in many cities.

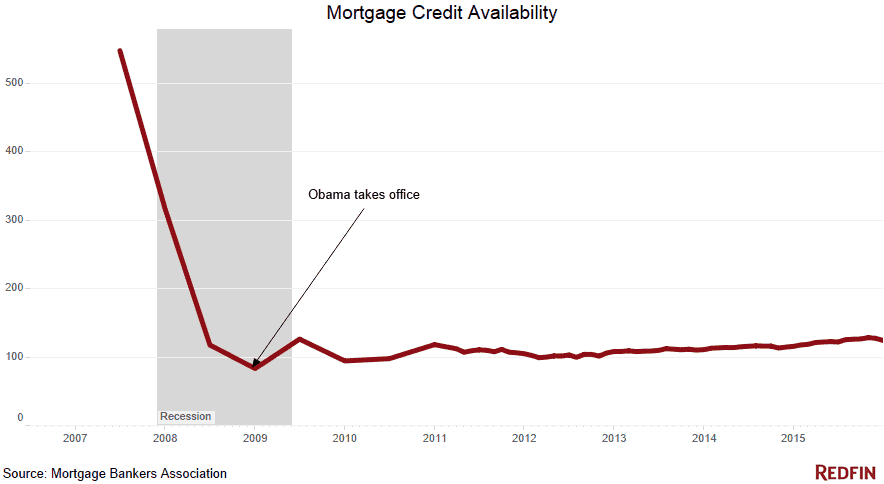

8. Fewer People Can Get Loans

After the meltdown, Congress went to great lengths to protect buyers from toxic mortgages. Unfortunately, that’s made even plain-vanilla loans harder to get, especially for first-time and self-employed borrowers. We’re still seeking the right balance, said Mike Fratantoni, chief economist at the Mortgage Bankers Association. On the bright side, there’s not much chance of another credit bubble. This chart says it all.

9. Taxpayers Are Knee-Deep In Mortgages

If you do have a home loan, it’s probably backed by the government. Nearly 74 percent of all mortgage dollars are funneled through the Federal Housing Administration, Fannie Mae, Freddie Mac and the Veterans Administration. In 2007, those agencies accounted for only 56 percent of home loans, according to Inside Mortgage Finance. Private lenders are just starting to tip-toe back into the market.

Where does that leave the state of housing? Approaching normal, but not there yet.

“Housing has come a long way and it’s moving in the right direction,” Redfin chief economist Nela Richardson said. “Still, for many middle class families home ownership remains a dream deferred by high prices, tight credit and stagnant wages.”

— With Taylor Marr