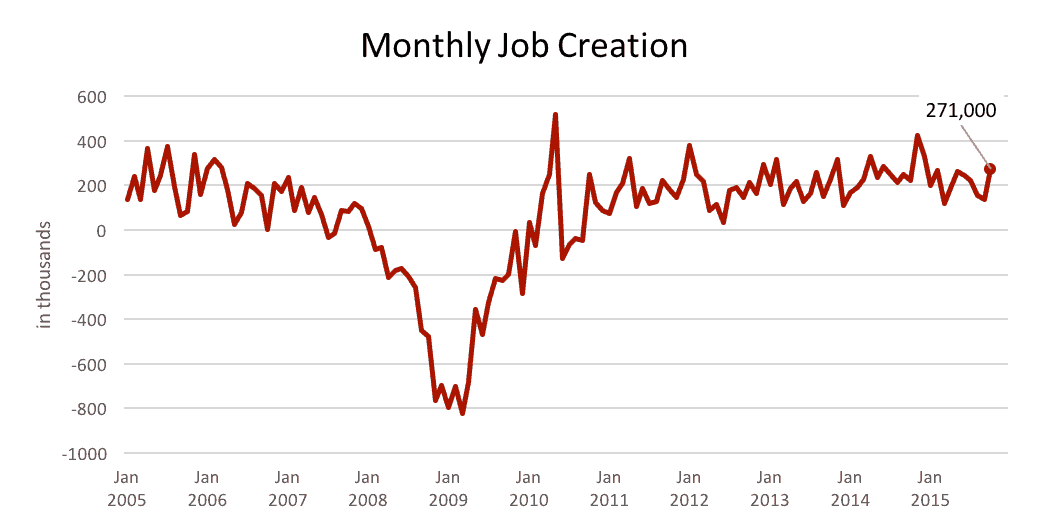

Employers added a whopping 271,000 jobs last month, more than anyone had predicted. Almost every sector of the economy improved, unemployment fell to its lowest since 2008, more people joined the labor market and wages are starting to rise.

In short, it was the best monthly jobs report we’ve had in almost a year.

Hiring improved in nearly every industry, with construction adding 31,000 jobs.

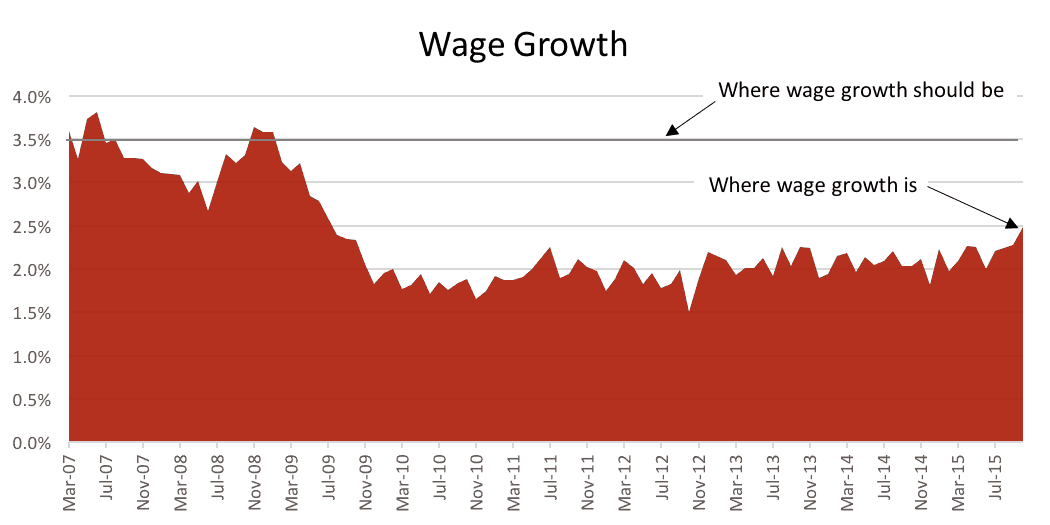

The happiest surprise was the increase in wages, which rose 2.5 percent from a year earlier, the biggest jump in six years.

That’s good, but it’s not good enough. We’ve been stuck at about 2 percent wage growth since the recession ended in 2009. According to the Economic Policy Institute, a liberal-leaning think tank, worker pay should be growing by about 3.5 percent a year.

Wages have a lot of catching up to do, and we still have too many discouraged and underemployed workers. But overall, we can’t complain about today’s report. It gives the Fed one more reason to raise rates in December.

“October has not been a good month for the nattering nabobs of negativity,” with auto sales, service sector growth and employment all coming in strong, said Neil Dutta, an economist at Renaissance Macro Research. “The U.S. labor market has given a green light to the Fed.”

A Fed rate hike doesn’t necessarily mean mortgage rates will rise. Even if they do, a gradual pickup won’t hurt the housing market. Remember this chart:

Lorraine.woellert@redfin.com

United States

United States Canada

Canada