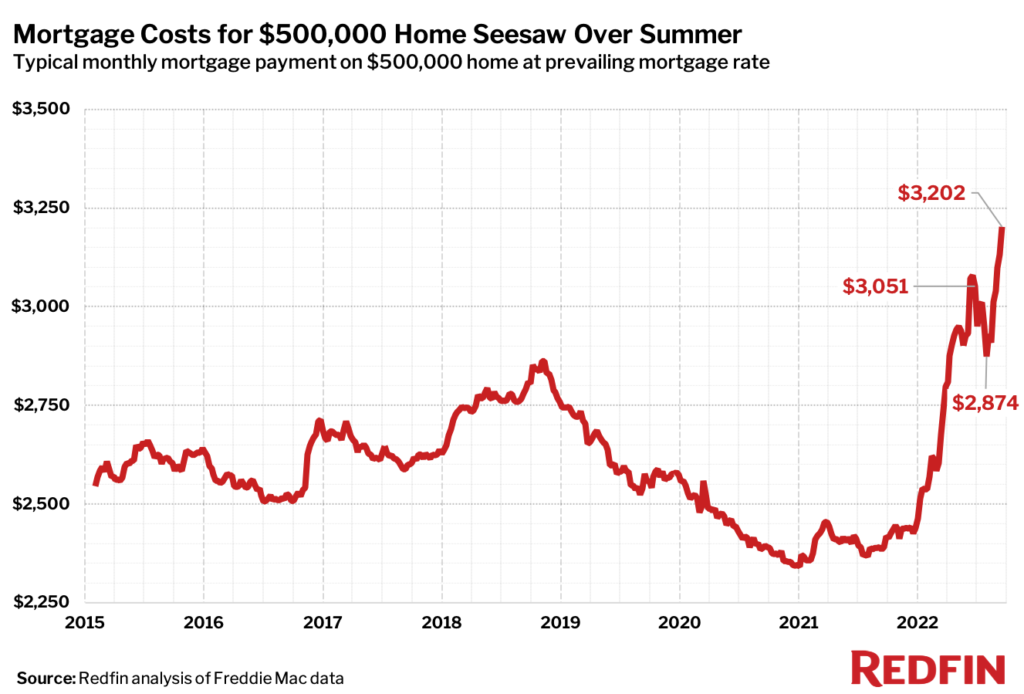

A house hunter looking for a $500,000 home saw their potential total mortgage payment fall by $64,000 from July to August, and then jump by $118,000 from August to September.

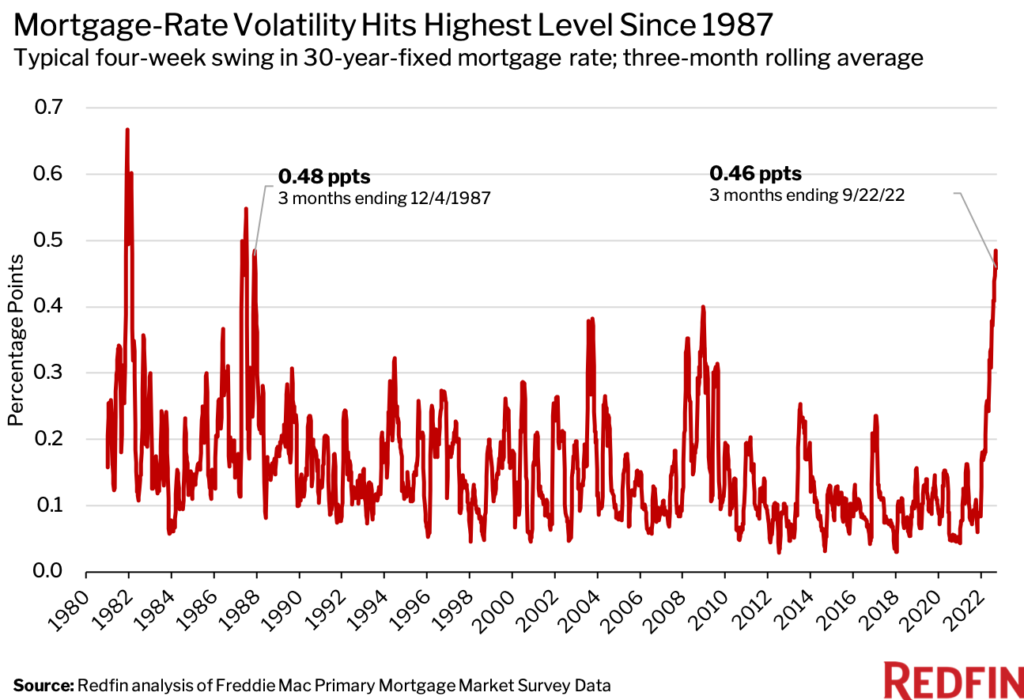

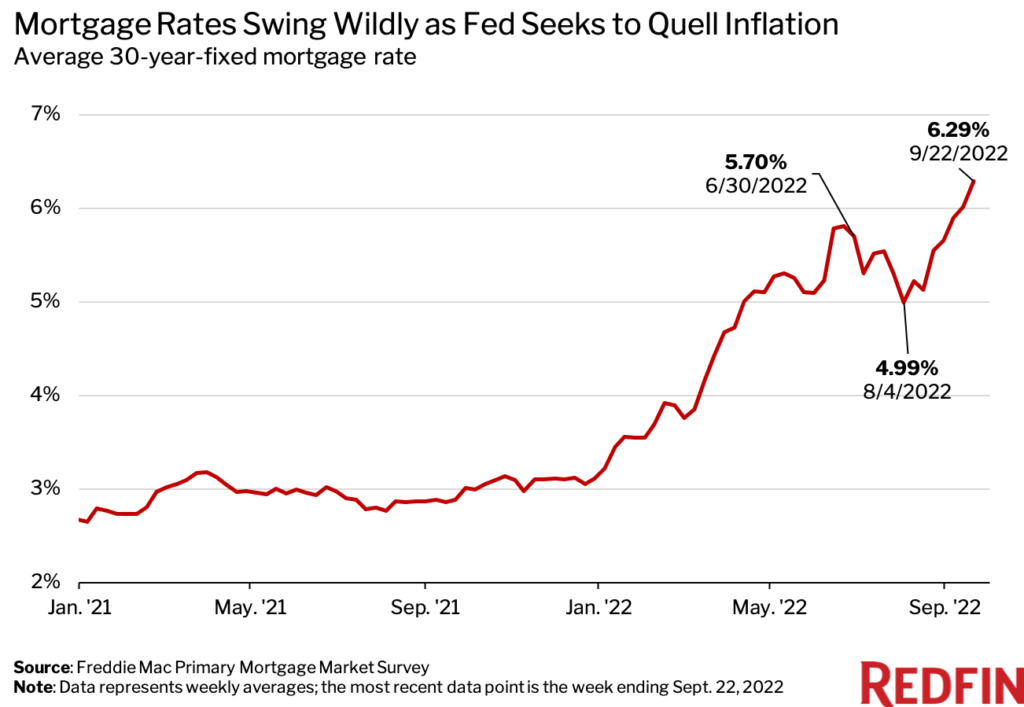

Seesawing mortgage rates, which have swung from nearly 6% to below 5% to above 6% in the last three months, are causing headaches for homebuyers. The typical house hunter who started searching in July and closed the deal on their new home in September saw their potential mortgage rate fluctuate by roughly half of a percentage point every four weeks. That’s the most volatile three-month period since 1987, when mortgage rates swung wildly after surging to a record high of nearly 19% earlier in the decade while the Fed worked to quell severe inflation.

Fast forward 35 years, and a new era of inflation and economic uncertainty has sent the average 30-year-fixed mortgage rate on another rollercoaster ride.

For a house hunter looking to buy a $500,000 home, this could mean that:

- When they started looking in early July, they expected their monthly payment to be $3,051. That equates to a total of $1.098 million over 30 years, assuming a 20% down payment and the prevailing 5.7% mortgage interest rate. Of that total payment, $435,777 is interest.

- When they found their dream home in early August, they expected their monthly payment to be $2,874. That equates to a total of $1.035 million over 30 years, assuming a 20% down payment and the prevailing 4.99% mortgage rate. Of that total payment, $372,143 is interest.

- When they locked in a mortgage rate for the home in late September, their final monthly payment turned out to be $3,202. That equates to a total of $1.153 million over 30 years, assuming a 20% down payment and the prevailing 6.29% mortgage rate. Of that total payment, $490,382 is interest.

In other words, the buyer’s total expected payment declined by about $64,000 (5.8%) from July to August, and then shot back up by about $118,000 (11.4%) from August to September.

“The challenges homebuyers face in today’s market go beyond the dwindling affordability caused by high mortgage rates and home prices,” said Redfin Deputy Chief Economist Taylor Marr. “The whiplash in mortgage rates between when homebuyers set their budget and when they make an offer is also making it extraordinarily difficult to plan ahead.”

Mortgage rates are seesawing because the Federal Reserve has been raising interest rates as it works to tamp down sky-high inflation. The Fed last week increased interest rates by three-quarters of a percentage point to a range of 3% to 3.25%—its third big hike in a row—and predicted they’ll reach 4.4% by the end of the year. While Freddie Mac’s widely followed weekly data now has mortgage rates at 6.29%—the highest since 2008—a separate daily gauge has them as high as 7.08%.

The volatility in mortgage rates will likely continue in the near term as the Fed seeks to combat inflation, but mortgage rates should fall in the next 12 to 18 months if inflation eases as expected, according to Justin Dimler of Bay Equity, Redfin’s mortgage company.

“The good news for people who can still afford to buy a home and are set on making a purchase now is that they should be able to refinance to a lower rate in a year or two,” said Dimler, a regional sales manager at Bay Equity in the Seattle area. “I advise house hunters who qualified for a loan one or two months ago to get requalified by their mortgage adviser because the change in mortgage rates may mean they’re no longer eligible to borrow as much as before.”

While refinancing may become an option for homeowners in the coming months, buyers today should be aware that refinancing can come with significant costs.

Methodology

Redfin measured mortgage-rate volatility by calculating the standard deviation for a rolling 3-month window of the 4-week change in the 30-year-fixed mortgage rate. The most recent datapoint covers the 13-week period from June 30 to Sept .22, 2022.

Mortgage-rate data comes from Freddie Mac’s Primary Mortgage Market Survey, which measures weekly averages of the 30-year-fixed mortgage rate.

For mortgage-payment calculations, we assumed a 20% down payment, 1.25% annual property-tax rate and a homeowner’s insurance rate equal to 0.5% of the purchase price.