Key takeaways:

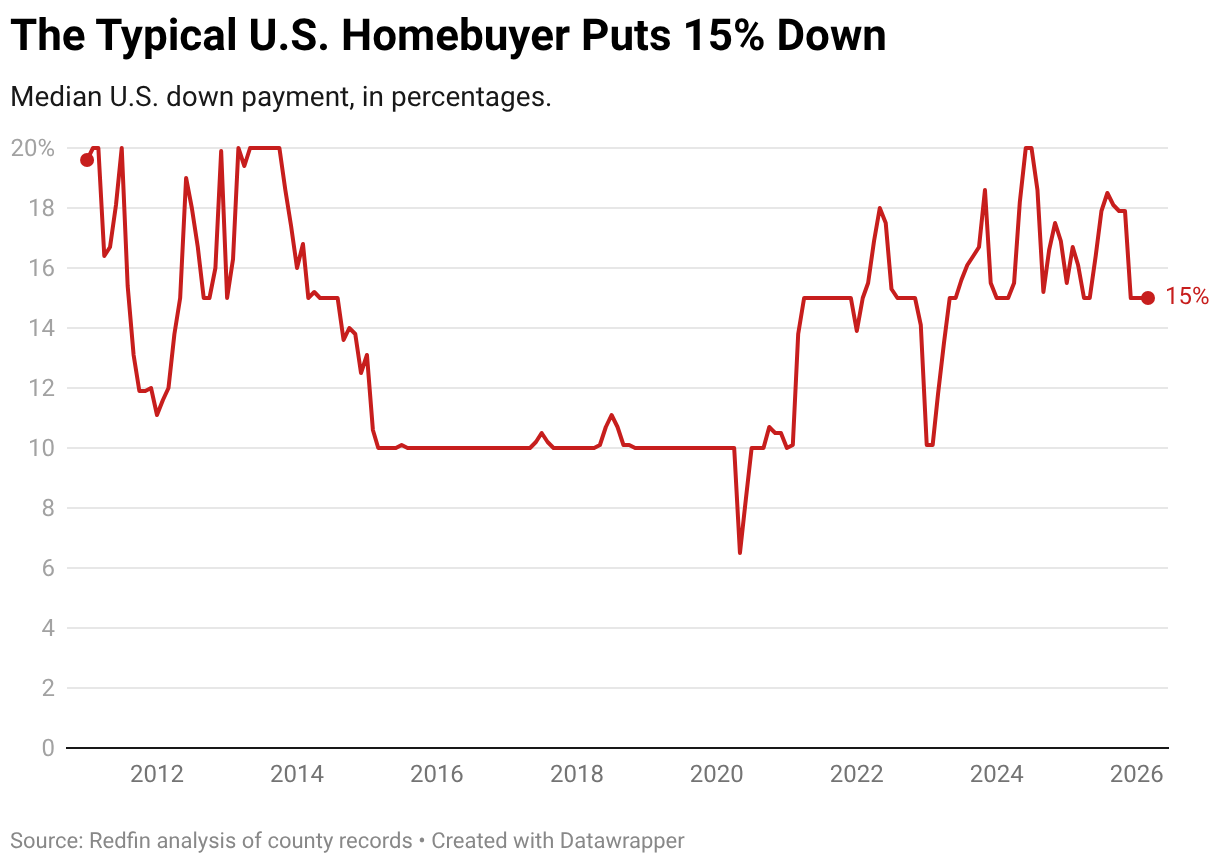

- The typical U.S. homebuyer puts down $64,000, equal to 15% of the purchase price.

- Most buyers put down less than 20%, with low-down-payment loan programs helping more buyers enter the market.

- The right down payment depends on your loan options, budget, and financial goals.

Saving for a down payment is one of the biggest obstacles between renters and homeownership, and in today’s market, it’s easy to see why. Home prices remain near historic highs, and the widespread assumption that you need 20% down makes ownership feel even further out of reach for many buyers.

But most buyers aren’t putting down 20%. The typical U.S. homebuyer put down $64,000 in March 2026, representing just 15% of the purchase price, down from 16.1% a year earlier. FHA and conventional low-down-payment loans now make up a growing share of purchases, reflecting how buyers are actively adapting to affordability pressures rather than waiting on the sidelines.

So how much do you actually need? Minimum requirements range from 0% on VA and USDA loans to 3–5% on most conventional and FHA options, with jumbo loans typically requiring 10% or more. But the minimum isn’t necessarily the right number for every buyer. Your loan type, credit profile, and financial goals all play a role.

What is a down payment?

A down payment is the money you pay upfront toward a home’s purchase price. It reduces the amount you borrow, which can lower your monthly payment and the total interest you pay over the life of the loan. It also gives you immediate equity in the home.

What’s the typical down payment on a house in 2026?

The typical U.S. homebuyer puts down 15% of the purchase price, or about $64,000. That’s well below the traditional 20% benchmark, reflecting how many buyers are adapting to today’s affordability challenges.

Rather than waiting to save a larger down payment, many buyers are using low-down-payment loan programs to get into a home sooner while preserving cash for closing costs, repairs, and emergencies.

Minimum down payment requirements by loan type

The amount you put down depends on the loan you qualify for and what makes financial sense for your situation. The table below shows minimum down payment requirements by loan type.

| Loan type | Minimum down payment for primary home |

| Conventional | 3-5% |

| Jumbo | 10-20% |

| FHA | 3.5% |

| VA | 0% |

| USDA | 0% |

Keep in mind these are minimums, not targets. Your actual down payment will depend on your lender’s requirements, your credit profile, and your goals.

How to calculate your down payment

The math is straightforward: multiply the home’s purchase price by your down payment percentage. Based on the median U.S. home sale price of $398,771 in May 2026, here’s what common down payment percentages look like in dollar terms:

| Down Payment % | Down Payment | Mortgage Amount |

| 3% | $11,963 | $386,808 |

| 3.5% | $13,957 | $384,814 |

| 5% | $19,939 | $378,832 |

| 10% | $39,877 | $358,894 |

| 15% (typical buyer) | $59,816 | $338,955 |

| 20% | $79,754 | $319,017 |

Not sure what works for your budget? Use Redfin’s mortgage calculator to estimate your down payment alongside your projected monthly costs.

How much should you put down?

The right down payment depends on your financial situation and goals.

If you’re a first-time buyer: Low-down-payment programs can get you into a home sooner without years of additional saving, though you’ll likely pay mortgage insurance and carry a higher monthly payment until you build enough equity.

If you’re using equity from a previous home sale: Repeat buyers often have the advantage of applying home sale proceeds directly toward their next purchase, which can support a larger down payment, lower monthly costs, and eliminate PMI.

If you want a lower monthly payment: A larger down payment reduces the principal you borrow, which lowers both your monthly payment and the total interest paid over the life of the loan.

If you want to preserve cash: putting down the minimum keeps more money available for closing costs, moving expenses, repairs, and emergency savings. In a high-price market, many buyers are making this tradeoff intentionally.

Is a 20% down payment mandatory?

No. While 20% is the traditional benchmark, most buyers today are putting down less. The typical U.S. homebuyer puts down about 15% of the purchase price. That said, hitting 20% does come with real advantages:

- No PMI: Conventional loans with 20% down waive private mortgage insurance, eliminating a monthly cost that protects the lender, not you.

- Lower monthly payments: A smaller loan principal means lower principal-and-interest payments and more monthly cash flow.

- Better interest rates: A lower loan-to-value ratio signals less risk to lenders, which can translate to a modestly lower rate and meaningful savings over time.

- Faster equity growth: More money down means you own a larger share of your home from day one.

- Stronger offer: In a competitive market, a higher down payment signals financial stability and a smoother path to closing.

For many buyers, though, waiting years to save 20% may not be worth delaying a purchase.

How are buyers funding their down payments?

Coming up with a down payment looks different for every buyer. The most common sources today include:

Personal savings: Still the most common source of down payment funds.

Equity from a previous home sale: Repeat buyers often use proceeds from a home sale to fund a larger down payment on their next home.

Gifts from family: A growing number of buyers, particularly first-timers, receive financial help from family members. Lenders generally require a gift letter confirming the funds don’t need to be repaid.

Down payment assistance programs: Federal, state, and local programs offer down payment assistance in the form of grants, forgivable loans, and low-interest second mortgages to help eligible buyers bridge the gap.

Frequently asked questions about down payments

Does a larger down payment affect my interest rate?

Sometimes. A larger down payment lowers your loan-to-value ratio, which can help you qualify for a better rate. But lenders weigh multiple factors, including your credit score, income, debt load, and loan type, so a bigger down payment alone doesn’t guarantee a lower rate.

What’s the difference between a down payment and closing costs?

Both are due at closing, but they serve different purposes. A down payment goes toward the purchase price and builds equity. Closing costs are separate fees covering lender charges, title insurance, prepaid taxes, and insurance. They typically run 2–5% of the loan amount. You’ll need to budget for both.

How does my credit score affect my down payment?

Your credit score helps determine which loan programs you qualify for and what minimum down payment may be required. FHA loans allow as little as 3.5% down with a score of 580 or above, but require 10% down for scores between 500 and 579. Conventional loans generally require a 620 or higher, with down payments starting at 3% for qualified buyers. A stronger score can also give you more flexibility, since lenders view a solid payment history as lower risk.

Can I use retirement funds for a down payment?

Yes, in some cases. Some accounts have provisions for first-time homebuyers, such as penalty-free Roth IRA contribution withdrawals, but rules vary by account type. Taxes, penalties, or long-term savings setbacks may apply. Speak with a financial advisor before tapping retirement funds for a home purchase.

How long does it take to save for a down payment?

It depends on your target and how much you can set aside each month. Based on Redfin’s data, the typical buyer puts down $64,000. At $1,000 per month in savings, that’s over five years. At $2,000 per month, closer to three. Starting with a specific target and working backward from your timeline is the most practical approach.

So, how much down payment do you need?

How much down payment for a house you’ll need depends on your loan type, savings, and what trade-offs make sense for your situation right now. The typical U.S. homebuyer puts down 15% of , but your number may be higher or lower.

Some buyers stretch to put down more and lower their monthly payment. Others keep cash in reserve and get into a home sooner. Neither approach is wrong. What matters is understanding your options well enough to make the choice that fits your goals.

If you’re ready to start running the numbers, Redfin’s mortgage calculator can help you estimate your down payment alongside your projected monthly costs. And when you’re ready to make a move, a Redfin agent can help you put together an offer that works for your market.