A social norm that ties homebuying to marriage is delaying women’s path to homeownership, even when they can afford to buy on their own.

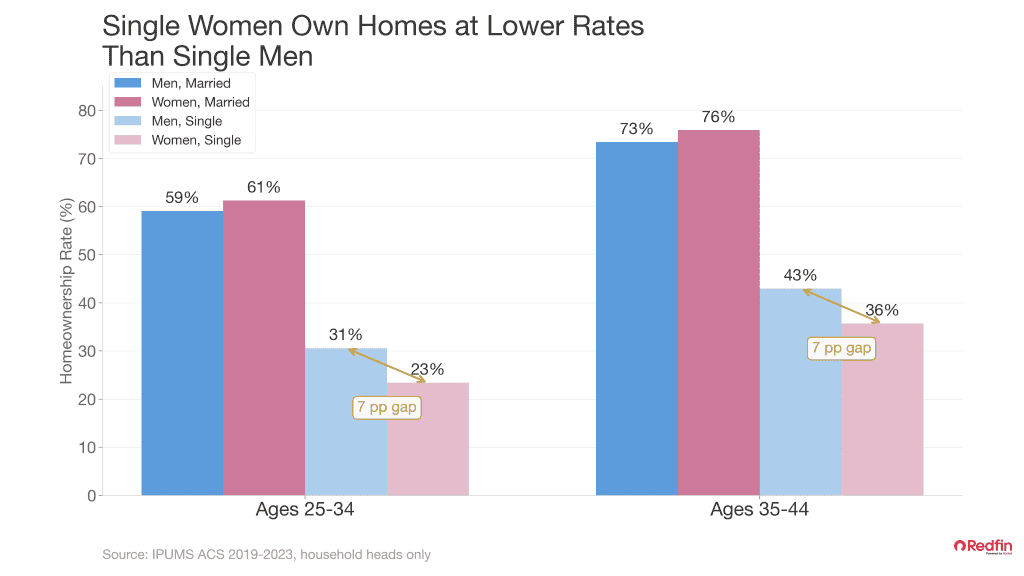

- 31% of single men ages 25-34 own their home, compared with 23% of single women the same age—a 30% gap.

- Marriage increases the likelihood of owning a home by 26%, even after controlling for combined household income.

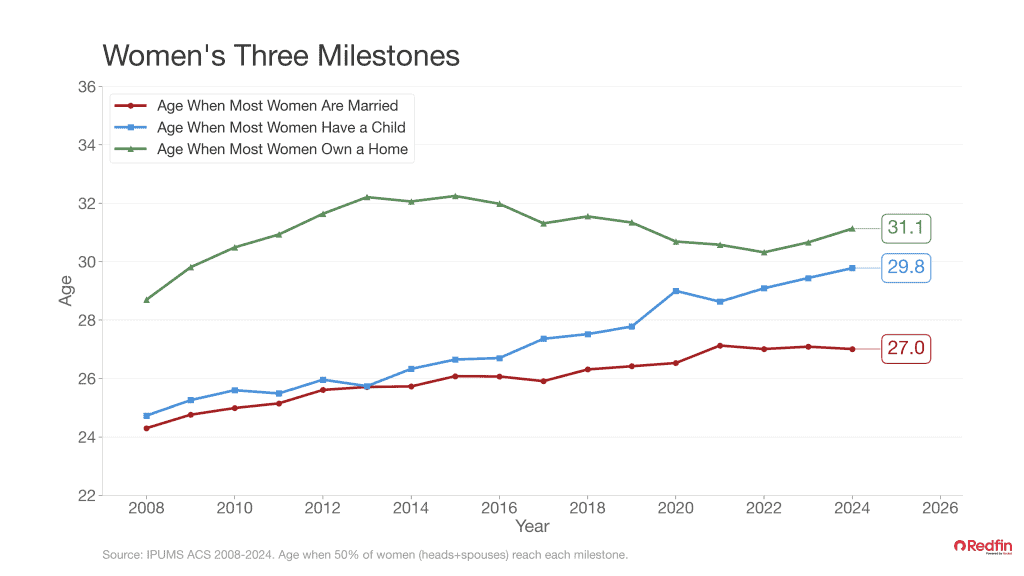

- Single women become homeowners at age 34, on average, while women who marry first reach homeownership at 31.

- The typical age at which American women have their first child has climbed from 25 in 2008 to 30 in 2024, and the typical age of homeownership has shifted from 29 to 31.

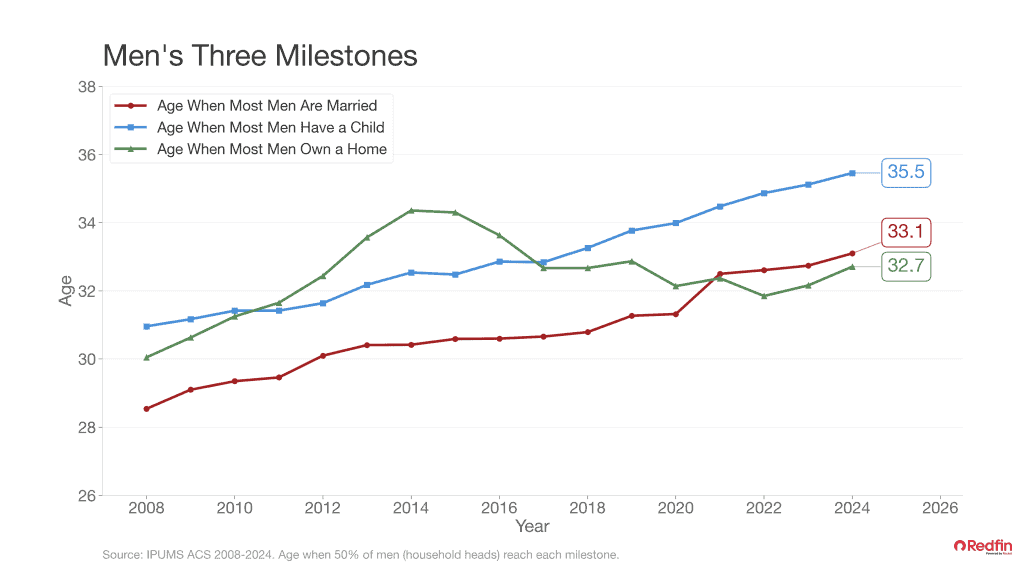

- Men, by contrast, now tend to buy a home at 33—before marriage and children, not after.

Men under 35 are roughly 30% more likely than single women to own a home, and most popular explanation—the gender pay gap—doesn’t fully hold up. Even when single women earn similar incomes to single men, they buy homes later. The reason has less to do with paychecks and more to do with a social timeline that still treats homeownership as something that comes after a wedding.

That timeline used to line up neatly. A generation ago, most American women were married by 24, had their first child by 25, and owned a home by 29. Marriage, kids, and a mortgage arrived as a synchronized package, often within a few years of each other. Those figures are based on the age at which half the population reached each major milestone according to data from the Census’ American Community Survey.

Those timelines have shifted. Today, most women are married by 27, have their first child by 30, and owns a home by 31. Each milestone has shifted later, but they haven’t shifted by the same amount—and that has consequences for who builds wealth, and when.

Men buy first. Women wait.

For men, the sequencing has flipped. The typical man now becomes a homeowner at 33—before marriage and before children. Buying a house has become a prerequisite for settling down, not a reward for it.

For women, the order is reversed. Marriage still tends to come before the keys. And the data show how costly that ordering is:

- Single women buy their first home at age 34.

- Women who marry first buy at age 31.

That’s a three-year head start for women who pair up before they sign a mortgage. Three years of equity, three more years of price appreciation, three more years of locked-in housing costs while rents keep climbing.

The gap isn’t just about combining two incomes. After controlling for combined household income, being married still raises the likelihood of homeownership by 26%. Something other than dollars is driving the pattern.

What’s actually holding single women back

The single-buyer homeownership gap is stark. Among 25- to 34-year-olds:

Income explains some of this, but not most of it. Single women in this age group earn less than single men on average, but the homeownership gap is wider than the income gap—and it persists even among single women who out-earn the typical single man.

A more uncomfortable explanation comes from the dating market. Research from University of Chicago economists finds that couples are less likely to form when the woman would out-earn the man. That single dynamic accounts for roughly 23% of the decline in marriage rates since 1970. In other words, financial independence on the part of women has measurable costs in the partner market.

It also has costs inside marriages that do form. According to research featured in The Ambition Penalty by Stefanie O’Connell found that women who out-earn their husbands are about 35% more likely to experience physical violence and 20% more likely to experience emotional abuse from their partner than women who don’t.

Buying a home is one of the most visible signals of financial independence a single woman can send. For some women, the (often unspoken) calculation is that buying alone might shrink the dating pool—or change the dynamic of a future relationship in ways they’re worried about. So they wait.

The cost of waiting

Waiting to buy is rarely free. Three years is enough time for home prices to rise meaningfully in most U.S. metros, for mortgage rates to move, and for a renter to spend tens of thousands of dollars on housing payments that don’t build any equity. A woman who buys at 34 instead of 31 isn’t just buying later—she’s typically buying a more expensive home, with less time for the mortgage to amortize before retirement.

The compounding effect is significant. Homeownership is still the single largest source of wealth for most middle-class American households. A three-year delay at the front end of a 30-year mortgage can translate into tens of thousands of dollars in lost equity by mid-career.

What single women considering a home should think about

The case for buying as a single woman isn’t that homeownership is right for everyone—it’s that the decision should be made on personal and financial readiness, not on a social script that says wait for a spouse.

A few things worth weighing:

- Can you stay put for at least five years?

Transaction costs on a home—agent fees, closing costs, moving costs—typically take several years of appreciation and principal paydown to recoup. If your job, family situation, or city plans are likely to change inside five years, renting may genuinely be the better financial choice. If they’re not, the math usually favors buying. - If you can afford it, don’t let a hypothetical partner’s reaction stop you.

A future spouse who is uncomfortable that you own a home is telling you something important about the partnership. The financial cost of waiting is real and measurable; the cost of buying is, in most cases, recoverable. - If you do partner up later, consider a property prenup.

A cohabitation or property agreement that spells out who owns what, who pays what, and what happens if the relationship ends protects the asset you built before the relationship started. This is true whether or not you ever marry. - Have a contingency plan.

Life shifts. If your circumstances change—a new job in another city, a partner who wants to move in, a desire for more space—a home you own can be rented out, refinanced, or sold. A home you didn’t buy can’t do any of those things.

Adulthood has unbundled

The deeper story here is that American adulthood has come unbundled. Marriage, homeownership, and parenthood used to arrive together. Now they don’t, and they don’t arrive in the same order for everyone.

For men, the sequence has rearranged itself in a way that builds wealth earlier: house first, family later. For women, the old script—marriage first, then the house—is hanging on, even as marriage itself happens later and less often. The result is that women, on average, start the wealth-building clock later than men, and single women later still.

The fix isn’t to push anyone into homeownership before they’re ready. It’s to stop treating a mortgage as something that requires a partner’s permission, or a partner’s signature, to make sense. If the financials work and the timeline works, the social timeline shouldn’t be the thing that holds the keys.

A longer version of this analysis was originally published on Daryl Fairweather’s Substack, Hate the Game, and a video version was published to YouTube.