Mortgage rates jumped to a 10-month high, spooking would-be homebuyers and sellers after a few weeks of solid demand.

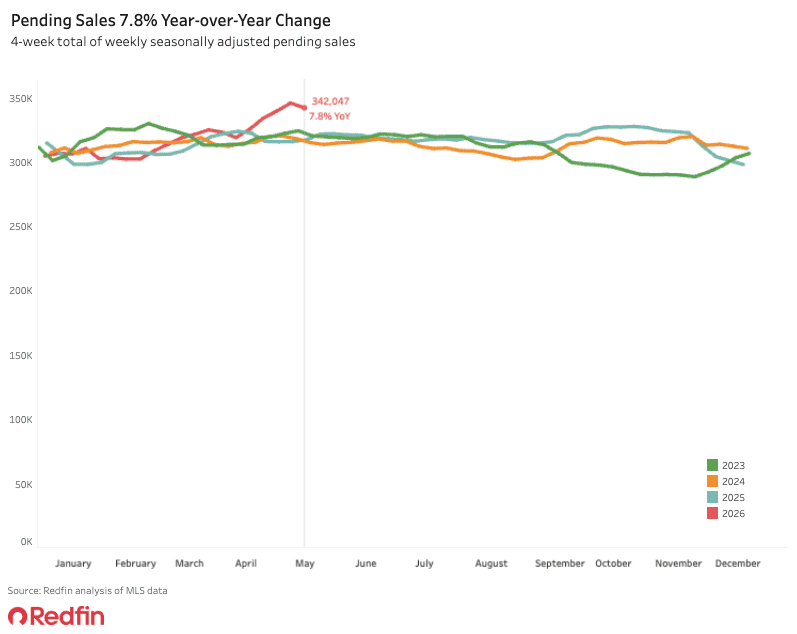

U.S. pending home sales fell 1.1% from a week earlier during the week ending May 17, the first decline since early April. Pending sales are still at their second-highest level since September 2022, but it’s notable that the jump we saw over the last several weeks is starting to reverse. Note that this data is seasonally adjusted.

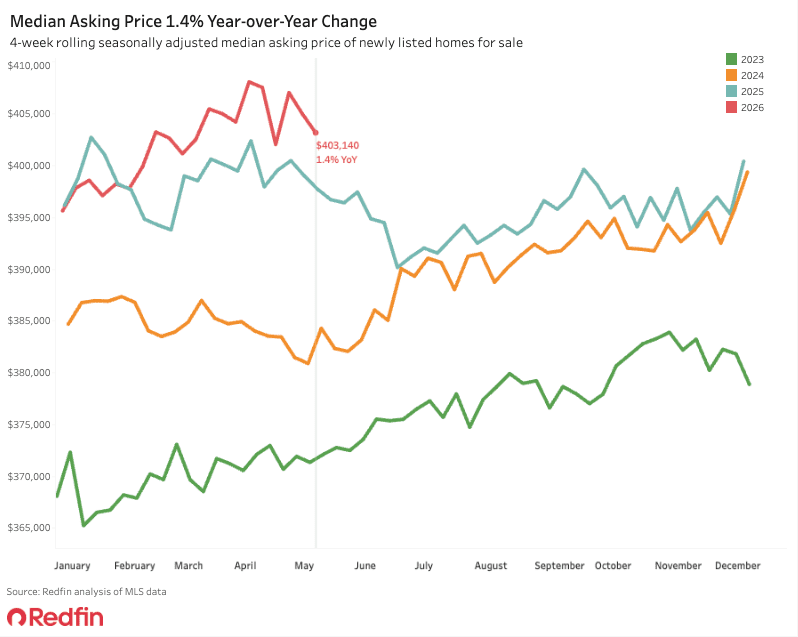

Additionally, mortgage-purchase applications declined 4% week over week. Homebuying demand fell because mortgage rates increased. The daily average mortgage rate hit 6.75% this week, the highest level since July. Prices are rising, too; the median asking price increased 1.4% year over year.

Pending home sales rose each week from early April to early May because of a strengthening job market and declining mortgage rates; the daily average rate dipped to the 6.3% range in mid-April. Now, rates have jumped due to the Iran war and the continued closure of the Strait of Hormuz spooking global markets.

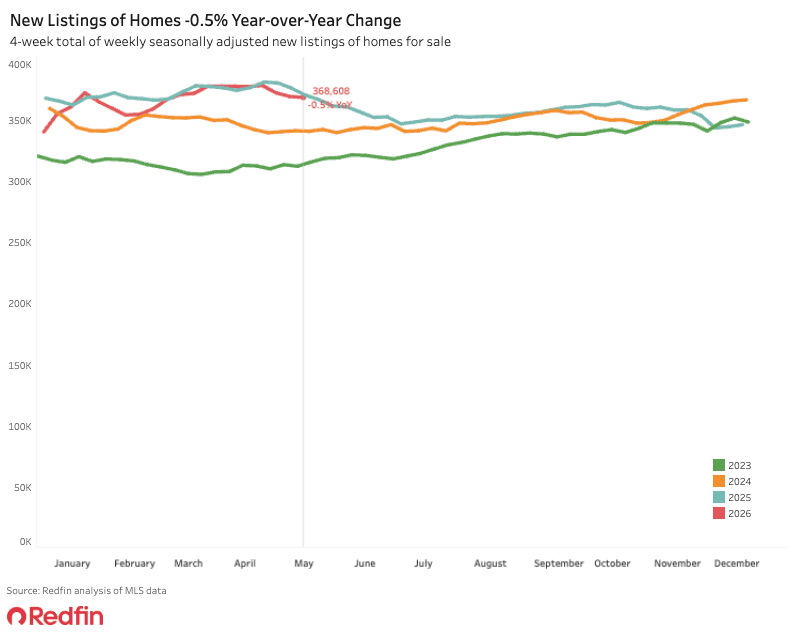

On the selling side, new listings declined 0.2% week over week on a seasonally adjusted basis. That marks the third straight week of new listings declining.

“Higher mortgage rates are scaring off some buyers, but that’s opening the door for others,” said Chen Zhao, Redfin’s head of economics research. “It’s already a buyer’s market, and this week’s jump in mortgage rates may give house hunters with stable incomes another opportunity to negotiate a home’s price down and get concessions from sellers.”

During a time of changing demand, sellers may consider a “coming soon” approach like Redfin Early Access, which allows them to test pricing strategies and gauge interest before formally listing on the MLS.

For Redfin economists’ takes on the housing market, please visit Redfin’s “From Our Economists” page.

Leading indicators

| Indicators of homebuying demand and activity | ||||

| Value (if applicable) | Recent change | Year-over-year change | Source | |

| Daily average 30-year fixed mortgage rate | 6.67% (May 20) | Highest level since July | Down from 6.99% | Mortgage News Daily |

| Weekly average 30-year fixed mortgage rate | 6.36% (week ending May 14) | Up from 6.23% three weeks earlier | Down from 6.76% | Freddie Mac |

| Mortgage-purchase applications (seasonally adjusted) | Down 4% from a week earlier (as of week ending May 15) | Up 8% | Mortgage Bankers Association | |

| Google searches of “homes for sale” | Highest level in 9 months (as of May 9) | Up more than 20% | Google Trends | |

| Touring activity | Up 29% from the start of the year (as of May 18) | At this time last year, it was up 36% from the start of 2025 | ShowingTime | |

Key housing-market data

| U.S. highlights: Four weeks ending May 17, 2026

Redfin’s national metrics include data from 900+ U.S. metro areas and are based on homes listed and/or sold during the period. Weekly housing-market data goes back through 2021. Subject to revision. |

|||

| Four weeks ending May 17, 2026 | Year-over-year change | Notes | |

| Median sale price | $398,653 | 2.2% | |

| Median asking price (seasonally adjusted) | $403,140 | 1.4% | |

| Median monthly mortgage payment (seasonally adjusted) | $2,597 at a 6.36% mortgage rate | -2.2% | |

| Pending sales (seasonally adjusted) | 342,047 | 7.8% | |

| New listings (seasonally adjusted) | 368,608 | -0.5% | |

| Active listings (seasonally adjusted) | 1,493,419 | 1.4% | |

| Months of supply | 3.5 | -0.1 pts. | 4 to 5 months of supply is considered balanced, with a lower number indicating seller’s market conditions |

| Share of homes off market in two weeks | 39.4% | Essentially unchanged | |

| Median days on market | 41 | +3 days | |

| Share of home listings with price drops | 18.8% | Down from 20% | |

| Share of homes sold above list price | 27.1% | Down from 28% | |

| Average sale-to-list price ratio | 98.9% | Down from 99% | |

|

Metro-level highlights: Four weeks ending May 17, 2026 Redfin’s metro-level data includes the 50 most populous U.S. metros. Select metros may be excluded from time to time to ensure data accuracy. |

|||

|---|---|---|---|

| Metros with biggest year-over-year increases | Metros with biggest year-over-year decreases |

Notes |

|

| Median sale price | San Francisco (9%)

Kansas City, MO (7.3%) Pittsburgh (5.6%) Detroit, MI (4.9%) Nassau County, NY (4.6%) |

Miami (-2.5%)

San Jose, CA (-2.1%) Orlando (-2%) Seattle (-1.8%) Fort Worth, TX (-1.4%) |

|

| Pending sales | West Palm Beach, FL (34.4%)

San Francisco (19.9%) Newark, NJ (15.4%) Minneapolis (15.4%) Pittsburgh (15.1%) |

Houston (-9.7%)

Seattle (-6.1%) Detroit (-2.2%) Philadelphia (-1.3%) Tampa, FL (-1.3%) Atlanta (-1.1%) |

Declined in 6 metros |

| New listings | Cincinnati (13.5%)

San Jose, CA (9.1%) Columbus, OH (9.1%) New Brunswick, NJ (8%) Warren, MI (7.7%) |

St. Louis (-16.4%)

Denver (-13.9%) Fort Worth, TX (-13.1%) Dallas (-11.9%) Riverside, CA (-11.3%) |

|

Refer to our metrics definition page for explanations of all the metrics used in this report.