Listings will rise and prices and rates will fall. But high housing costs will remain a problem for young families, which will increase demand for large rentals and force President Biden to make affordability a cornerstone of his reelection bid.

We’re starting to see signs of a shift toward a buyer’s market as pandemic-driven inflation takes its last gasps, mortgage rates come down and more people list their homes for sale. We expect these trends to continue in the new year, ushering in a season of hope for aspiring homebuyers.

And there’s more reason to be optimistic about 2024, when we expect to see an acceleration of consumer-friendly changes to the way Americans buy and sell homes.

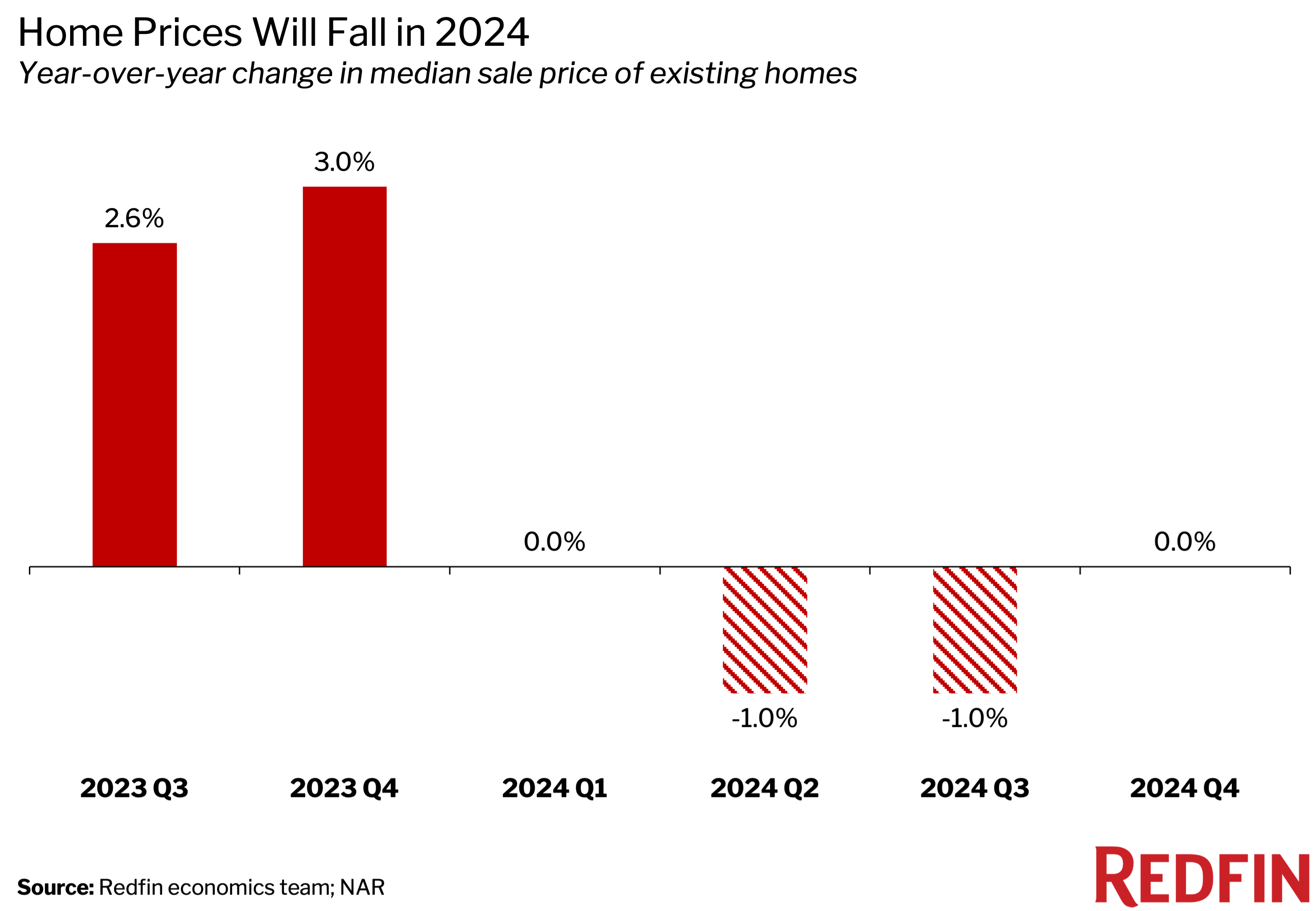

Prediction 1: Home prices will fall 1%

Prices will fall 1% year over year in the second and third quarters, when the home-selling season is in full swing. That will mark the first time prices have declined since 2012, when the housing market was recovering from the Great Recession, with the exception of a brief period in the first half of 2023.

That’s a favorable shift for buyers: Prices are ending 2023 up around 3% year over year, and the typical homebuyer’s monthly payment is only about $150 shy of its all-time high. Home prices will still be out of reach for many Americans, but any break in the affordability crisis is a welcome development nonetheless.

Prediction 2: New listings will tick up

Home prices will fall because supply will rise more than demand. We’ve recently seen a double-digit annual increase in homeowners contacting Redfin for help selling their home, alongside a small drop in requests from prospective buyers.

Listings will climb from 2023’s record low as the mortgage-rate lock-in effect eases. Nearly all mortgaged homeowners have a rate below the current level. Many are starting to accept that we won’t see rates in the 3s or 4s anytime soon, and they want to sell before prices fall. Redfin agents report that homeowners in places like South Florida, where prices have soared the last few years, are deciding to cash out on their equity and move to more affordable areas.

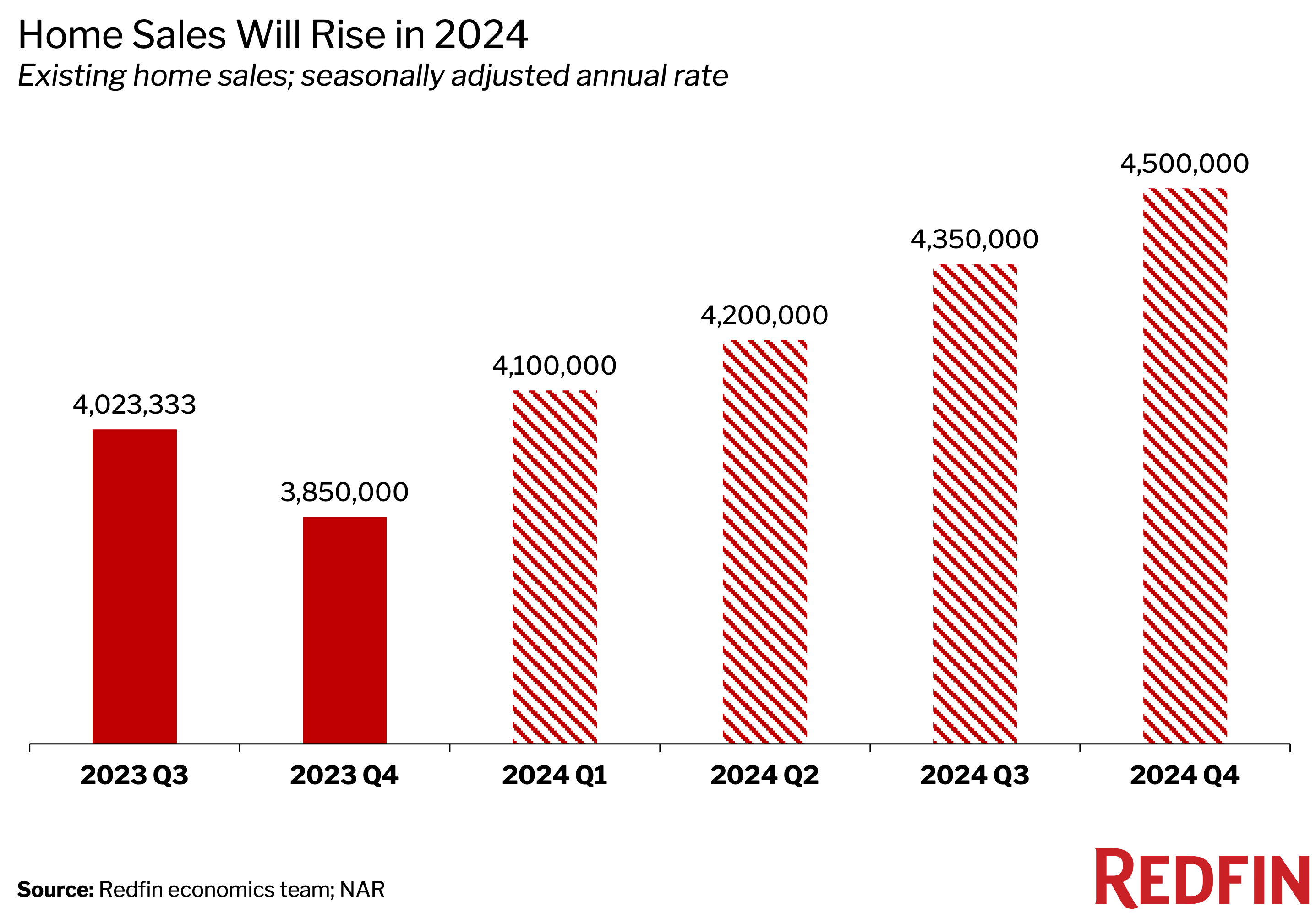

Prediction 3: Home sales will increase and end the year up 5%

In the first quarter, existing home sales will be on pace for 4.1 million total in 2024, up from an annual pace of 3.85 million in the fourth quarter of 2023. Sales will continue rising throughout the year; they’ll be on pace for a total of 4.5 million by the fourth quarter. Home sales will speed up throughout 2024 as affordability improves and more homes hit the market.

Overall, we expect 4.3 million sales in 2024, up 5% year over year. A crucial difference between 2024 and 2023 will be sales gaining momentum throughout the year instead of losing momentum.

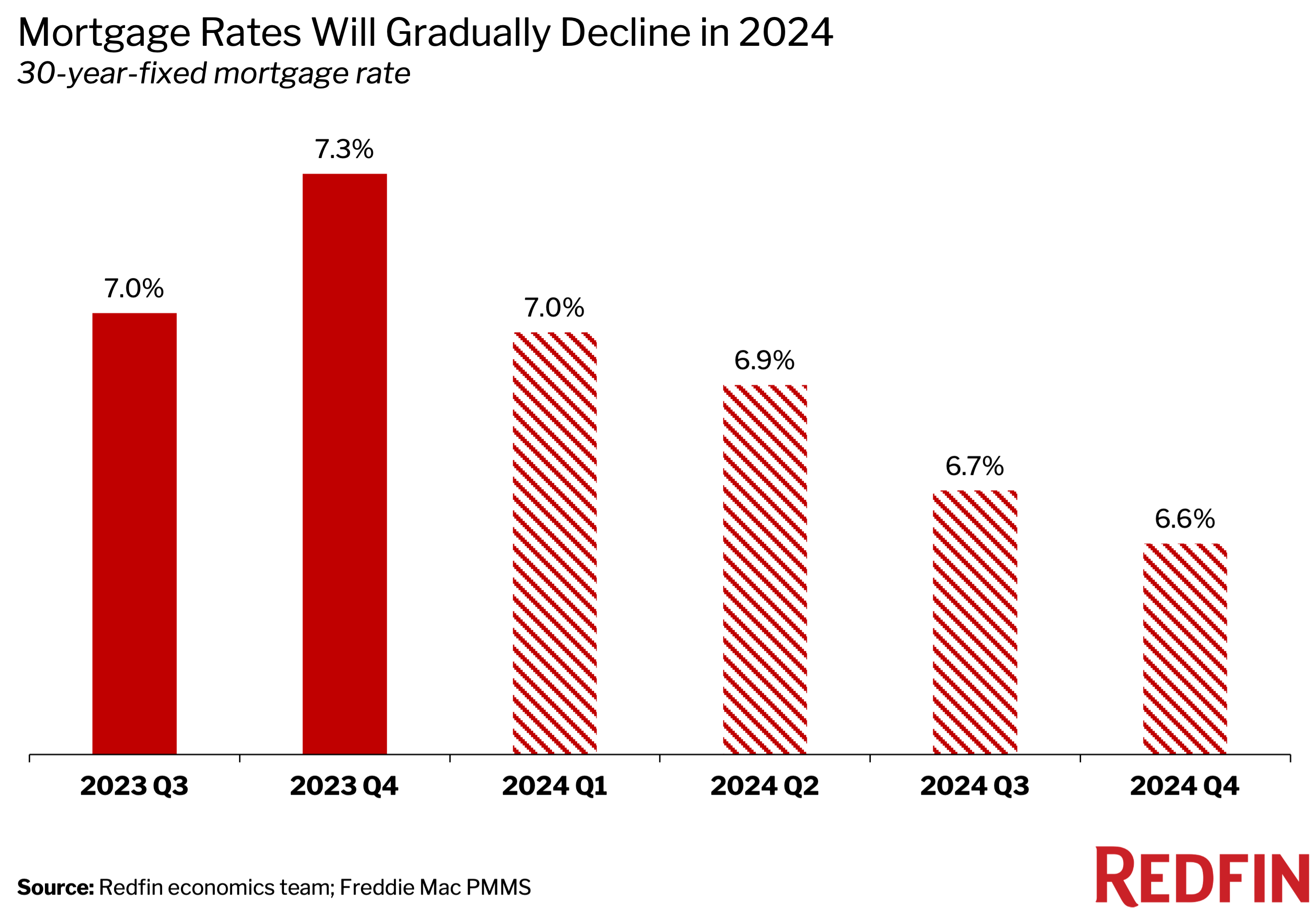

Prediction 4: Mortgage rates will steadily decline–but remain above 6%

We predict the average 30-year mortgage rate will linger at 7% in the first quarter, then decline throughout the year. Mortgage rates will fall to about 6.6% by the end of 2024. The gradual decline in rates combined with the small dip in prices will bring homebuyers some much-needed relief.

Mortgage rates are likely to remain well above pandemic-era record lows because financial markets increasingly believe the country will avoid a recession in 2024. The Fed will likely keep interest rates at their current level at the start of the year even though inflation is largely under control. But then they’re likely to cut rates two or three times starting in the summer, which is why mortgage rates will decline as the year goes on.

Prediction 5: Change will come to the real estate industry

An industry that has been mostly impervious to change is now changing quickly, a trend that will accelerate in 2024. For the first time in Redfin’s near-20-year history, our agents reported widespread discounting among our competitors in 2023, if not in the fee publicly offered to the buyers’ agent, then in commission refunds or in private listing agreements. As newspapers and real estate portals publish more information about commissions, homebuyers in 2024 will become even more aware of how much an agent costs, and less apologetic about negotiating commissions.

And rather than hiring their own agent, many homebuyers will work directly with the listing agent. This has long been common when the listing agent works for a builder, but with inventory low and competition among agents high, more re-sales are now being handled entirely by the listing agent, often for thousands less than what the buyer would pay if a second agent were involved.

The possibility of legal action will accelerate this trend in 2024, as the U.S. Department of Justice considers whether listing agents should be involved in setting the fee paid to a buyer’s agent. A DoJ suit could take years to litigate, and may never even be filed, but brokerages are already scrambling to prepare for a future in which all or most of the fees from a sale are earned by one agent, not two.

These changes, which Redfin has often fought for, will be good for consumers, who will have more choices about which services to pay for and how much to pay.

Prediction 6: Renting will lose its stigma

Demand for large rental apartments and houses will climb as more young families embrace the renter lifestyle. We’re already seeing signs that young people are redefining the American Dream; nearly one in five millennials who responded to a 2023 housing survey believe they’ll never own a home. For some, renting is not a choice: Nearly half of those survey respondents said homes for sale are too expensive and a similar share said they can’t afford to save for a down payment. But others just prefer renting: 12% said they aren’t interested in homeownership and 7% said they don’t want to put in the effort to maintain their own home.

With prices so high, buying a home doesn’t offer the same financial upside to young millennials and Gen Zers as it did baby boomers and Gen Xers. Rather than shelling out cash on agent fees, interest on a loan, property taxes, insurance and maintenance, many will decide that renting and investing their money in other ways makes the most sense.

We expect prices of large rental units to climb next year as supply fails to meet demand. However, there will be downward pressure on prices for smaller rentals because there are more of them and a backlog waiting to hit the market. Builders, who have focused on building smaller apartment units since around 2019, will start to increase their investment in family-friendly rental units.

Prediction 7: Biden has a housing problem, which could hurt his re-election bid

Home prices are up more than 20% since President Biden took office. That’s a problem for his re-election bid: A recent poll found that 65% of voters disapprove of Biden’s handling of the economy, with lack of housing affordability likely a major factor. Even though the overall economy is strong, high housing costs are making many Americans feel poor. That’s especially true for young people who don’t yet own a home. And even though affordability will become less of a problem in 2024, many Gen Z and millennial voters will be playing financial catch-up for a while.

We expect President Biden and his opponents to make splashy housing policy proposals to try to lure voters who are unhappy with their economic prospects. Democrats are likely to focus on subsidizing down payments for first-time homebuyers, promoting inclusionary zoning and funding housing vouchers, which are all popular with liberal voters. Republicans are more likely to focus on reducing regulations that limit development.

There’s more in store for 2024: Big price declines in coastal Florida, a wave of boomerang migration, local governments enact policies to improve housing affordability

- Prices will fall a lot in some metros and rise in others

-

-

- We expect prices to fall fairly significantly in parts of coastal Florida, including North Port and Cape Coral. That’s partly because prices there surged during the pandemic, leaving a lot of room to fall, and partly because increasing risk of climate disasters is making those areas less desirable and home insurance more expensive.

- Prices are likely to rise in affordable metros that are more climate resilient than a place like coastal Florida such as Albany, NY, Rochester, NY and Grand Rapids, MI.

-

- People will decide where to live based on in-office policies, climate risk and affordability concerns

-

-

- There will be a wave of boomerang migration, where remote workers who fled expensive job centers for more affordable places return to where they came from. See: Tech employees moving back to Seattle from Boise, ID as companies enforce in-office policies; people leaving coastal Florida as disaster-insurance costs rise.

- Many priced-out young Americans will move in with their boomer parents, oftentimes along with children of their own, creating more 3-generation households.

-

- Local governments will focus on housing affordability

-

-

- More local governments will adopt a land-value tax to make homes more affordable and promote building.

- Like presidential candidates, congressional candidates will focus on housing affordability. They will introduce policies similar to those in cities and states that have made progress, like Minneapolis, Oregon and California, which are among the places that have ended most single-family-only zoning.

- The U.S. government will encourage cities and states to build more housing; for instance, they may take a more active role in financing new construction.

-

- More homeowners will use their home as an ATM, pulling out cash to cover credit card debt and home renovations

Our 2024 predictions are set against a backdrop of economic unpredictability. Our outlook could change due to uncertainty in other areas: financial market volatility, the course of the wars in Europe and the Middle East and the U.S. presidential election. To that end, below are upside and downside scenarios for our predictions on mortgage rates, home prices and sales:

- Upside scenario: Weekly average 30-year fixed mortgage rates drop into the 5% range. That could happen if the U.S. economy falls into a recession. While higher unemployment would drag down demand, the effect of lower mortgage rates would outweigh that effect, pushing prices up by about 3% and sales up to about 5 million.

- Downside scenario: Mortgage rates surpass 8%–which hasn’t happened since the early 2000s–and stay high. That could happen if the Fed holds interest rates steady all year. Home prices could fall 5% or more, and sales could drop into the 3.5 million range.