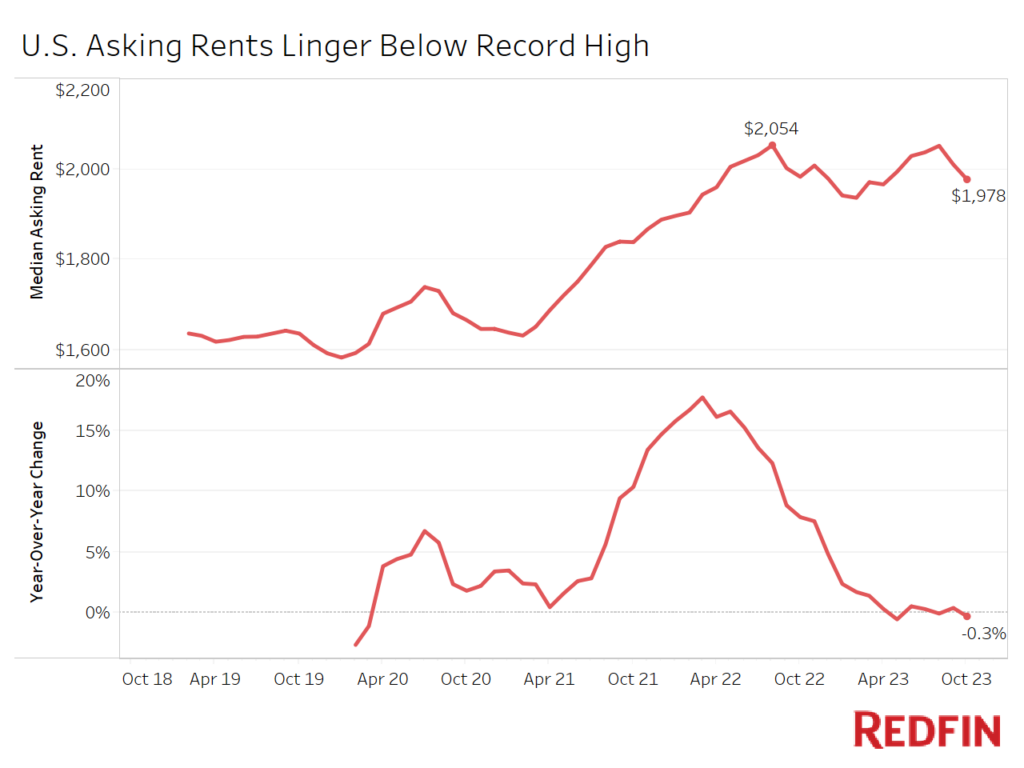

Asking rents were little changed from a year earlier for the seventh-straight month as an increase in new units hitting the market drove up vacancies, making it harder for landlords to raise prices.

The median U.S. asking rent in October was $1,978, little changed (-0.3%) from a year earlier, but down 3.7% from the $2,054 record high set in August 2022. It fell 1.6% from a month earlier, which is typical for this time of year.

October marked the seventh straight month in which the median asking rent was little changed from a year earlier. The rental market has flattened out following a rollercoaster ride during the past two years; rent growth skyrocketed during the pandemic as housing demand surged, and then rapidly slowed last year as inflation and economic uncertainty intensified.

“Rents in Phoenix have pulled back,” said local Redfin Premier real estate agent Heather Mahmood-Corley. “During the pandemic, you’d see five people applying for the same unit, and you’re not seeing that anymore. Rentals are sitting on the market for longer. Landlords are willing to work with tenants on lease terms and concessions because consumers are just more skittish these days. A lot of folks are staying where they are instead of moving because there’s so much uncertainty in the economy and in the world.”

The rental market has cooled in part because there’s a lot of new inventory, which means landlords are grappling with rising vacancies and have less leverage to raise rents. That’s the reverse of what’s happening in the for-sale housing market, where prices are rising due to an inventory shortage. Listings in the for-sale market have plunged because surging mortgage rates have prompted many homeowners to stay put, as moving would mean trading in their low rate for a much higher one.

The jump in supply isn’t the only factor that has caused rents to flatten; slowing household formation has also contributed—along with rising affordability challenges driven by the pandemic surge in rents, which rendered apartments in some areas unaffordable for many renters.

Still, there has been enough rental demand to prevent rents from declining significantly. That’s partly because high mortgage rates and low for-sale inventory are keeping many would-be homebuyers in the rental market. The median asking rent in October remained 20.8% higher than it was in October 2019, before the pandemic.

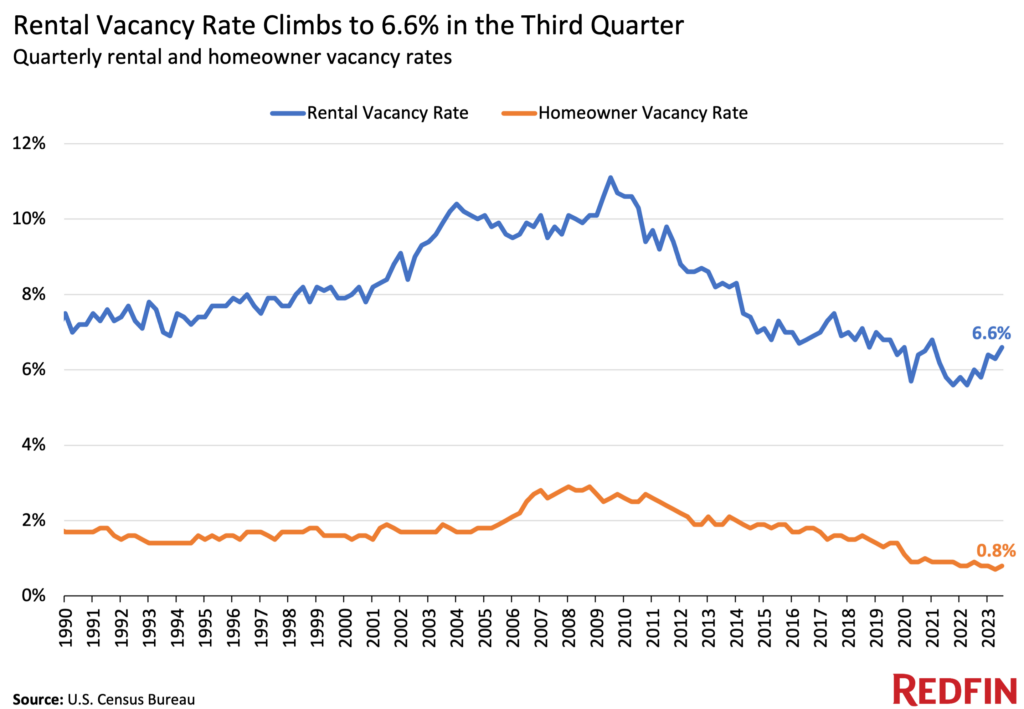

Rental Vacancies Rise as More Units Come on the Market—But Building Slowdown Could Bolster Rents

The rental vacancy rate hit 6.6% in the third quarter—the most recent period for which data is available—the highest level since the first quarter of 2021. By comparison, the homeowner vacancy rate was 0.8%—the second lowest level in records dating back to 1956 (the lowest was in the prior quarter).

Rental vacancies are on the rise because renters have an increasing number of options to choose from. The number of completed apartments in the U.S. rose 4.9% year over year in the third quarter to a seasonally adjusted annual rate of 1.2 million, one of the highest levels of the last three decades. Completions did fall from the prior quarter, when they hit 1.4 million, the highest level in over 35 years.

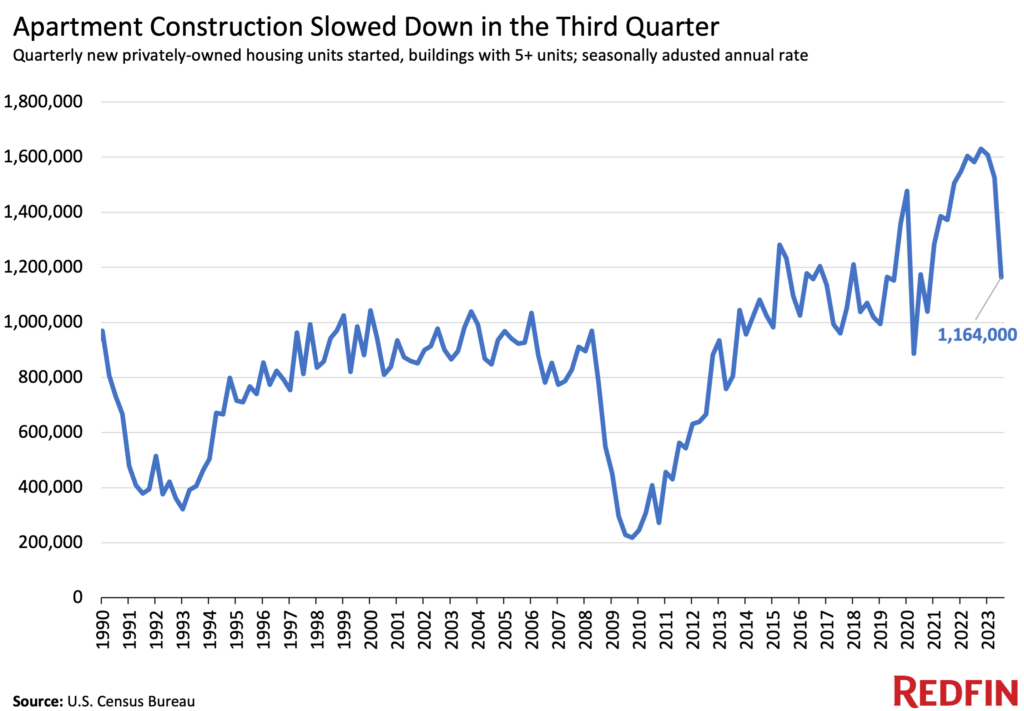

But the number of apartment buildings on which construction has started plunged 26.5% year over year in the third quarter to a seasonally adjusted annual rate of 1.2 million. That’s the biggest drop since 2010 and the lowest level since 2020. Building starts are a leading indicator of what’s happening in the housing market, whereas building completions are a lagging indicator.

The slowdown in apartment construction could ultimately bolster rent prices. Building has slowed due to rising interest rates, sluggish rent growth and possibly overbuilding in some areas.

Rents may also hold up relatively well for two-plus bedroom apartments next year as prospective house hunters opt to rent instead of buy due to elevated mortgage rates.

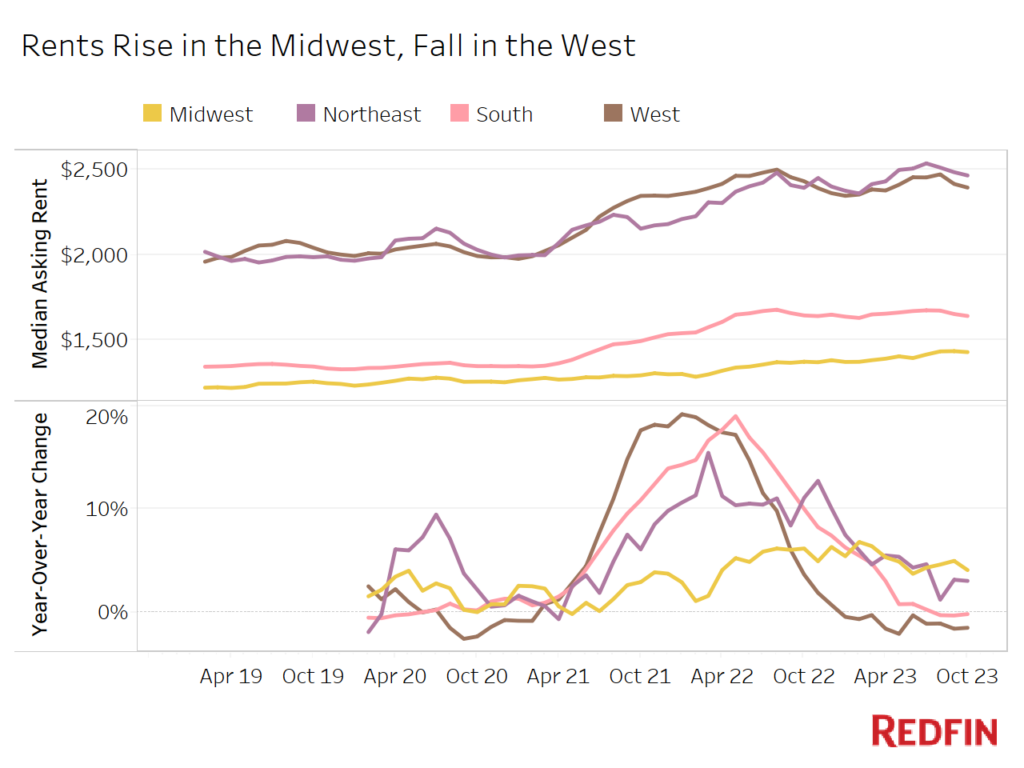

Rents Fall Most in the West, Rise Most in the Midwest

The median asking rent in the West fell 1.5% to $2,392, and in the South was little changed, down 0.2% to $1,642. Meanwhile, asking rents grew 4.1% to $1,430 in the Midwest and rose 3% to $2,463 in the Northeast.

Rents are climbing fastest in the most affordable region and falling fastest in one of the least affordable, which makes sense at a time when housing affordability is becoming a problem for more American families. Research shows that a near-record share of house hunters are leaving their metro when they move, many in search of a more affordable place to live.

Another reason the rental market has softened substantially in the West and South is that those markets saw outsized growth during the pandemic. Rents skyrocketed as people flooded into Sun Belt cities including Phoenix, Miami and Dallas. But once the rental boom in those regions cooled, prices had relatively more room to fall. Apartment construction in the Sun Belt has also been especially robust, contributing to the cooldown in rents.

While rents in the West and South have been cooling, these regions’ rental markets have started to stabilize in recent months as the impact of the pandemic price boom moves further into the rearview mirror.

Methodology

Asking price data includes single-family homes, multi-family units, condos/co-ops and townhouses from Rent.com and Redfin.com.

Redfin has removed metro-level data from monthly rental reports for the time being as it works to expand its rental analysis.

Prices reflect the current costs of new leases during each time period. In other words, the amount shown as the median rent is not the median of what all renters are paying, but the median asking price of apartments that were available for new renters during the report month.