Digital currencies are becoming an increasingly common payment method as millennials rush the housing market.

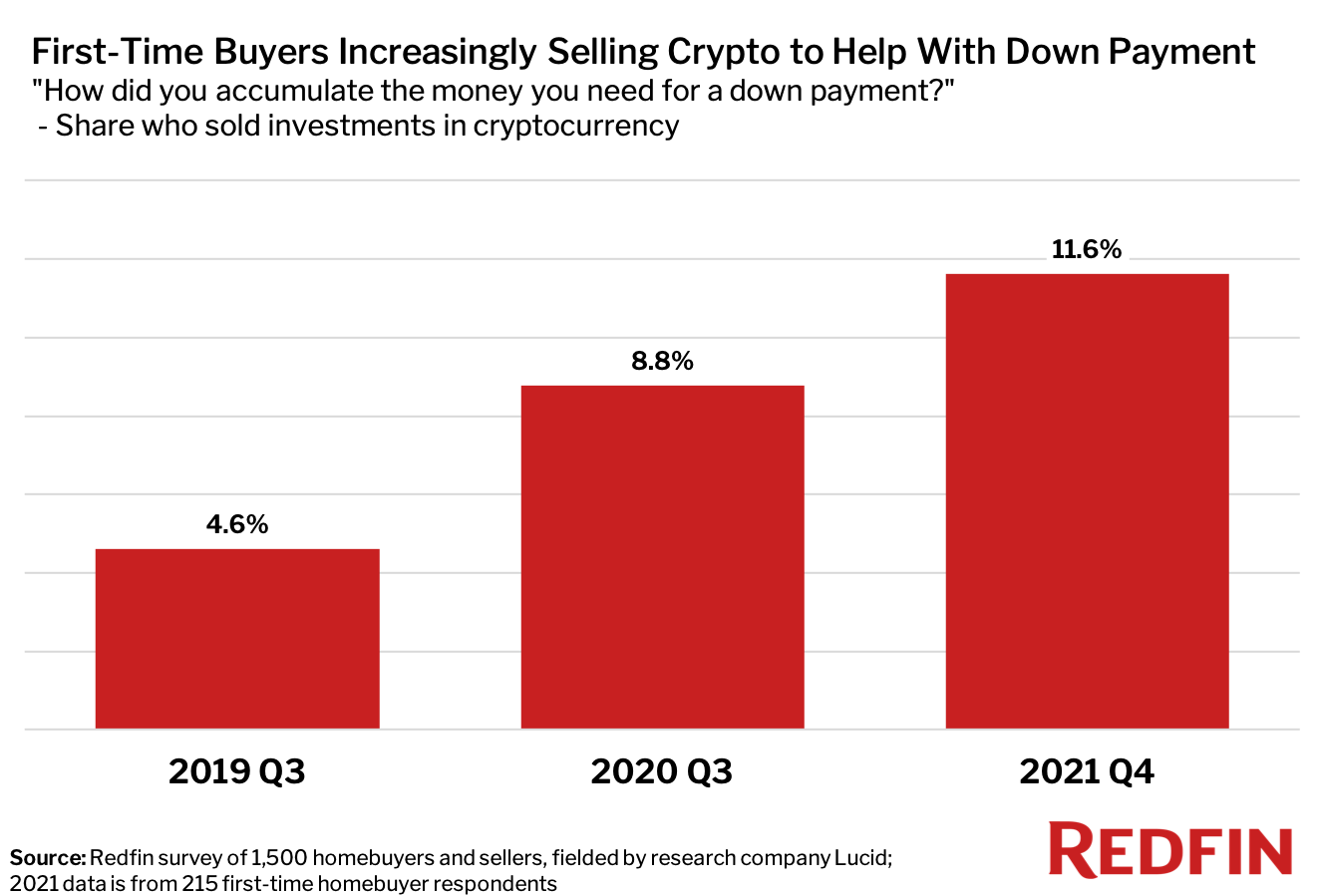

One in nine first-time homebuyers (11.6%) surveyed in the fourth quarter said selling cryptocurrency helped them save for a down payment. That’s up from 8.8% in the third quarter of 2020 and 4.6% in the third quarter of 2019.

This is according to a Redfin-commissioned survey of 1,500 U.S. residents planning to buy or sell a home in the next 12 months. The survey, which was fielded to a representative sample of the American population, was conducted by research technology company Lucid from Dec. 10 to Dec. 13, 2021. Respondents were not made aware that Redfin was the sponsor of the research.

This report focuses on the 215 of those 1,500 respondents who answered the question “How did you accumulate the money you need for a down payment?”—a question we only posed to participants who indicated they were planning to buy their first home in the next year. The most common response was “saved directly from paychecks” (52%), while less common answers included “cash gift from family” (12%) and “pulled money out of a retirement fund early” (10%).

“With extra time and a lack of exciting ways to spend money, many people began trading cryptocurrencies during the pandemic,” said Redfin Chief Economist Daryl Fairweather. “Some of those investments went up in smoke, but others went ‘to the moon,’ or at least rose enough to help fund a down payment on a home.”

Bitcoin, the world’s largest digital currency, hit a record high of nearly $69,000 in November. Ether, the second most valuable cryptocurrency, also reached an all-time high, though both coins have since lost some of those gains. With surging home prices leading to larger down payments, some buyers are finding non-traditional ways to cover the cost and compete with other bidders.

“Crypto is one way for people without generational wealth to win a lottery ticket to the middle class,” Fairweather said.

Digital currencies are also likely on the rise as a payment method among homebuyers because millennials and Generation Z are taking up an increasing share of the U.S. housing market. Millennials, who own more cryptocurrency than other generations, now account for more than half of new mortgages.